Value investing has quietly reasserted itself across most of the world, with Trustnet analysis showing it has outperformed growth in 19 of 24 developed markets and many emerging markets over the past five years.

The past decade is typically seen as one where the growth style of investing has dominated markets across the board, punctuated by the occasional period when value investing came to the fore only to recede again.

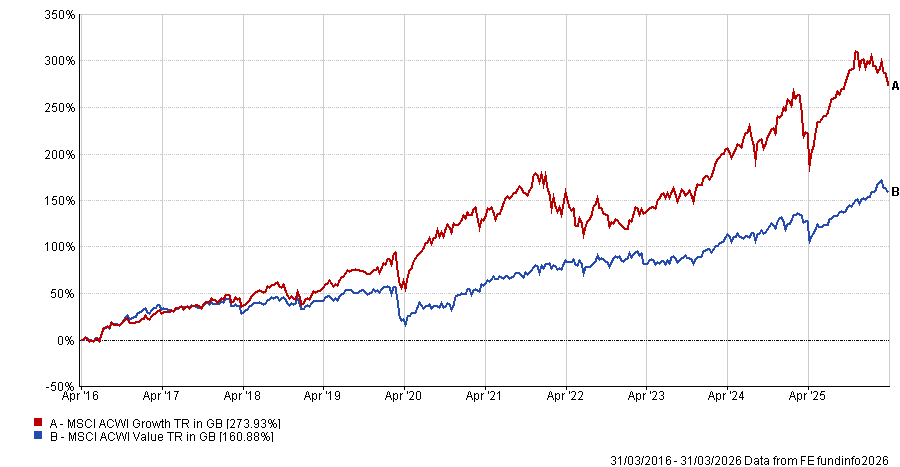

Growth’s outperformance is reflected in the 10-year numbers. FE fundinfo data shows the MSCI AC Growth index has made a 273.9% total return in sterling over the decade to the end of March 2026, compared with just 160.9% from its value counterpart.

Performance of global value and growth indices over 10yrs

Source: FE Analytics. Total return in sterling between 1 Apr 2016 and 31 Mar 2026.

The same trend can be seen on a more granular level as well. The developed markets-focused MSCI World Growth index made 295.6% over the same period, versus 166.5% from MSCI World Value; MSCI Emerging Markets Growth is up 140.1% compared with MSCI Emerging Markets Value’s 120%.

Growth investing targets companies expected to increase earnings faster than the market average, typically trading at premium valuations in anticipation of future profits. Value investing, on the other hand, seeks companies trading below their intrinsic worth on the basis that the market has mispriced their fundamentals and the gap will eventually close.

The decade of growth investing’s dominance rested largely on ultra-low interest rates following the 2008 financial crisis, which reduced the discount rate applied to future earnings and inflated the present value of companies whose profits lay years ahead. Compounding this, investors paid progressively higher price multiples for those earnings, while value stocks concentrated in energy, financials and industrials delivered earnings that consistently disappointed.

But the past few years have become more favourable to value investing, owing to higher interest rates, elevated inflation and improving sentiment towards industrials, energy and financials.

Over five years, the MSCI AC Growth index is still outperforming MSCI AC Value but by a much slimmer margin: 63.2% versus 62.4%. Value investing beats growth in emerging markets over the same period but growth remains dominant in developed markets.

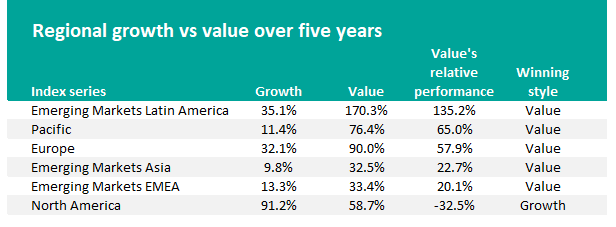

But drilling down even further shows that value investing has actually led in most areas apart from one very notable exception. Value has made higher returns in Latin America, the Pacific region, Asia, Europe and EMEA.

Source: Finxl. Total return in sterling between 1 Apr 2016 and 31 Mar 2021.

The exception is the MSCI North America Growth index, which has made 91.2% over the past five years while MSCI North America Value is up just 58.7%. US stocks account for around 95% of the MSCI North America index.

US growth stocks benefitted from the same ultra-low interest rates and investor willingness to pay higher multiples for future profits as the global market. At the same time, a small group of US mega-cap technology companies generated profits that consistently exceeded already elevated expectations, validating premium valuations and pulling the growth index higher.

This matters because these US mega-cap tech stocks have grown to be an increasingly large part of global indices, skewing their biases towards growth. For example, the five largest stocks in the MSCI AC World are Nvidia, Apple, Microsoft, Amazon and Alphabet; the US accounts for 63.2% of the index while more than one-quarter is in information technology companies.

The picture therefore changes when we look at global stocks excluding the US. The MSCI ACWI ex USA Growth index has made 22.9% over five years – significantly behind the 74.8% from the MSCI ACWI ex USA Value.

The gap between the two styles has been largest in the MSCI Emerging Markets Latin America indices, where value has outpaced growth by 135.2 percentage points. Brazil is a major contributor to this (value index up 193.8% versus 8.4% from growth) as the country’s stock market is skewed toward classic value sectors like commodities, energy, financials and industrials, which have benefitted from persistently high interest rates.

Peru, Poland and United Arab Emirates are the other emerging markets where the value index has beaten growth by more than 100 percentage points over the past five years but growth has outperformed value in some emerging markets, including the Philippines, Thailand and Saudi Arabia.

The most notable is Taiwan, where the growth index is 110 percentage points ahead of its value counterpart; this is down to the fact that Taiwan Semiconductor, the growth stock that produces more than 90% of the world's most advanced semiconductor chips, accounts for close to 60% of the wider MSCI Taiwan index.

Source: Finxl. Total return in sterling between 1 Apr 2016 and 31 Mar 2021.

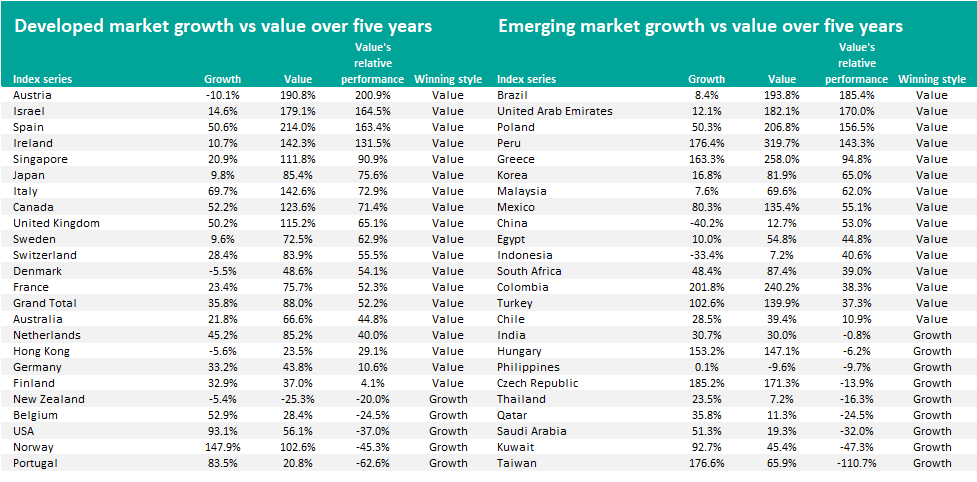

Over in developed markets, Austria has the biggest gap between growth and value stocks – 200.1 percentage points in favour of value. There are only five stocks in the MSCI Austria index, which has a 75% weighting to financials and another 16.3% to energy – both seen as value sectors.

Value has outperformed growth over the past five years in 19 of the 24 countries classed as developed markets by MSCI. Israel, Spain and Ireland join Austria in having more than 100 percentage points between their value and growth indices.

As well as the US, growth has beaten value in New Zealand, Belgium, Norway and Portugal.

To look at the long-term picture, WisdomTree analysed nearly a century of US market data in early 2025. It found that growth’s recent dominance is the exception rather than the rule, driven in large part by sentiment-driven multiple expansion rather than earnings alone.

When that dynamic has played out before, most notably during the late 1990s technology bubble, the reversal was abrupt and painful for growth investors. Value, by contrast, has historically provided a degree of resilience precisely because it does not depend on investors maintaining confidence in elevated valuations, the firm argued.

Brian Manby, senior associate for research at WisdomTree, said: “In our view, today’s style debate has grown too dismissive of value despite contrary evidence across decades of market history and recent performance regimes. Today, growth investors remain unbothered by historically high multiples, no doubt infatuated by the perceived limitless potential of AI and companies’ willingness to spend handsomely to harness it.

“We encourage investors to be cautious and discerning of prevailing growth valuations, especially if they’re neglecting value allocations in the process. Any change in sentiment could unwind the growth leadership cycle and valuations may be the catalyst.”