Making money every year is hard, yet the VT De Lisle America fund is on a seven-year streak of positive returns – and is in the black again so far in 2026. Only 20 funds in the IA North America sector have achieved this feat, totalling just 11% of the 182-strong peer group with a long enough track record.

Manager Richard de Lisle said: “A lot of people dropped the ball in, say, 2022 because they might have had the Magnificent Seven. We got away with that, partly because we don’t have any technology. That helps.”

But the other aspect is his barbell approach, which involves buying unloved companies in sectors with contrasting fortunes.

For example, consumer cyclicals are paired with energy companies. If energy prices rise, this improves the oil stocks’ profits but is poor for consumer cyclicals, as higher gas prices heavily impact consumers’ ability to buy other goods.

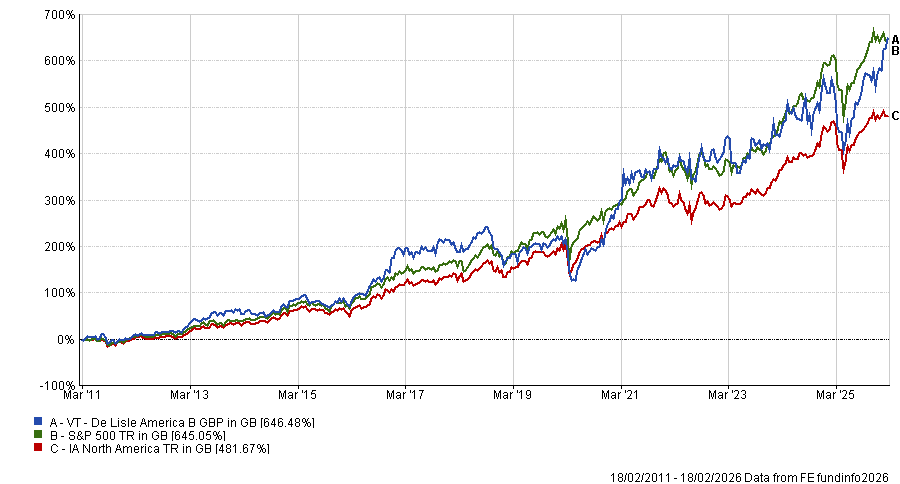

This approach has helped the fund not just in recent years, but over the long term as well. Despite investing in small-cap value stocks, it has beaten the dominant large-cap S&P 500 over 15 years and has made returns broadly in line with the market over five years (3 percentage points shy) and 10 years (5 percentage points off the index).

Performance of fund vs sector and S&P 500 over 15yrs

Source: FE Analytics

Below, de Lisle outlines why momentum is a better indicator for value stocks than growth companies; uses McDonald’s as an example for why quality investing is struggling; and explains why fund managers aren’t old enough.

What is your process?

We use every forward indicator we can find and then we fit that into long‑term demographic themes. The number one key metric is the net shareholder yield, which is defined as dividend yield plus net change in share count. That's the main one. That’s number one.

Number two, not far behind in weight, is price‑to‑sales ratio. It used to be the best forward indicator but it's dropped to number two on the quant work we have.

With interest rates going lower, companies were encouraged to buy back shares more aggressively. Some companies were really dropping the share count, which gave them good forward price action and helped the indicator that’s narrowly in front [net shareholder yield].

On group metrics, which are really important, value is number one, momentum is not far behind at number two and a bit of a distant third is size.

Momentum works much better with value than growth because it shows something’s changing, whereas with growth it's just confirming the straight line of earnings is ongoing.

Why do you use price-to-sales and not price-to-earnings?

Number one: it works. And number two: you can’t cheat on sales. We demonstrated that recently with McDonald's.

If you look over 40 years or more, McDonald's earnings trot along a pretty steady straight line but earnings growth is greater than sales growth.

How do you do that? You can introduce drive-throughs, automate the menu and so on, but you cannot increase margins forever.

McDonald's sales peaked in 2014, so to keep those rates of growth going, you need to keep plugging earnings. So what these companies do is they hollow out the company by buying back stock.

These stocks have done well for 40 years. Has something changed and are fund managers prepared for this?

Fund managers aren’t old enough, even those in their 70s. There was a market trend of P/E [price-to-earnings] expansion from 1980 to 2020. In 1980, Coca‑Cola was on 9x earnings, Kellogg’s was on 7x, and they all had the world ahead of them.

Now they're all on about 26-27x and yet their growth rate is slower. They've reached the extent of their growth.

What worked for fund managers was the gentle rise of P/Es as interest rates fell for 40 years. The pandemic pushed yields even lower and gave the cycle a final push. There were negative mortgage rates in Denmark, negative Nestlé corporate bond yields – you had the maximum potential for P/E expansion.

Then came the turn. So the game changed – the game that worked for 40 years. These fund managers with their great growth stocks – they’re not going to work as well. P/Es will diminish. That’s what has happened over the past three or four years alongside the AI [artificial intelligence]-driven narrowing of the market.

Why should investors pick your fund?

Because we've beaten the S&P 500 index over 15 years despite being in small‑cap value, which has been a very bad place to be.

I think where we are positioned is unusual, because other funds in our space became extinct in the great disinflation. That now means our competition will tend to be new funds.

As a small-cap value manager, has the AI large-cap boom been difficult for performance?

We're not interested in traditional growth stocks because we think they're overvalued. And we have thought that for many years. So it was difficult for us to outperform when the multiples on growth stocks just got higher.

The earnings growth rate of Apple – from the introduction of the iPhone – is only 12% a year, but the stock has gone up at a much higher rate because of P/E expansion.

That whole environment was difficult for us but that’s going the other way now and so is coming our way.

What has been your best stock in recent years?

Cameco, a big uranium producer. We bought that at $9.80 in 2018. Our target was $70. When the price touched $60 we revised the target to $100 on the basis that this uranium cycle is stronger than the last one.

We don’t have a target at the moment. I don’t know where it’s going, because we're sort of entering the acceleration phase of an uptrend. What happens in these sort of mining situations is you slowly get a feeding frenzy going.

Little things drop in which are bullish, then something else drops in and then uranium correlates with the data‑centre play and it correlates with precious metals. Soon, it sends everyone crazy and the uptrend accelerates. So it’s in that phase at the moment.

And the worst?

A stock called MasterBrand, which makes kitchen cabinets. It was spun off by Fortune Brands. We bought it because it was a spin [off], which is a good, outperforming asset class that you only really have in America.

Existing holders dump it and Wall Street doesn’t pick it up for years, so you tend to have an under‑priced stock. It takes about five months following the spin to get all the people who have received it from the parent company out.

We bought it at $14, it went up to $20, so we took it up to 3% of the fund. It’s now back to $12. It has hurt us.

What went wrong?

We are bullish on housing but there has been a setback. It comes down to the fact that nobody’s buying any kitchen cabinets because consumer confidence is at an extraordinarily low level, even though GDP is rocking along.

That has hurt our consumer cyclicals. We are bullish on consumer cyclicals but that’s a slight problem if everyone’s not spending. We’re gently selling some at the moment but I haven't given up hope on it.

What do you do outside of fund management?

I’ve got two boys. I have managed to get quite good at Latin because my son is reading classics. So we've sort of been doing it together for the past 10 years. I love spending time with my wife. Apart from that, I have no other interests. I am a nightmare. Even when young, I would go to sleep in the theatre or the cinema.