With Labour battling political instability at home, a fragile economy and a drift in the polls towards parties on both flanks, chancellor Rachel Reeves used her latest Spring Statement to project steadiness.

Her update was designed to be a non-event, having previously stated that she would not use the statement to make policy changes.

Instead, she attempted to reassure the public, repeatedly stating that her economic plan is “the right one for Britain”.

Matthew Amis, investment director at Aberdeen, said: “Chancellor Reeves wanted a non-event and we got a non-event – fiscal headroom slightly higher if you squint, gilt issuance maybe a touch higher, long issuance maybe a touch higher but nothing in the detail that will be driving gilt yields.”

Faye Church, senior planning direct at Rathbones, added that the statement was intentionally unexciting, noting that “predictability is a policy tool in its own right”.

The Office for Budget Responsibility (OBR) also avoided drama this time around, publishing its report only after Reeves had finished speaking, following the accidental release of its figures in the run-up to last year’s Budget.

It confirmed that Reeves’ fiscal headroom has risen from £21.7bn to £23.6bn, helped by stronger tax receipts.

Growth is now expected to come in at 1.1% in 2026 (down from 1.4% in November), before rising to 1.6% in both 2027 and 2028, while inflation is forecast to fall from 3.4% in 2025 to 2.3% by year-end, with January’s rate down to 3%.

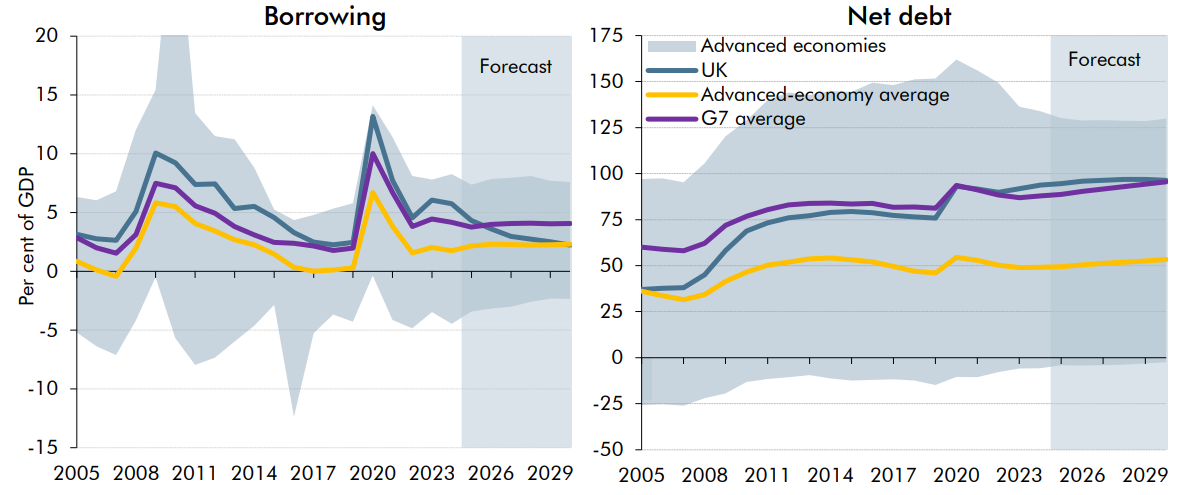

Borrowing is projected to fall from 5.2% of GDP in 2024-25 to 4.3% this year and fall further to 1.6% by 2030-31, leaving borrowing in the final year £8bn lower than previously forecast.

Public-sector net debt is forecast to rise from 94.5% of GDP in 2025-26 to a peak of 96.5% in 2028-29, before easing to around 95% by 2030-31 – around one percentage point lower than the November forecast.

The OBR noted that UK public debt as a share of GDP has nearly tripled over the past 20 years and the cost of servicing this debt has risen sharply – from 1.7% of GDP in 2019-20 to 3.6% in 2024-25 – reflecting significantly higher borrowing costs.

As such, the UK currently faces the highest 10‑year bond yields in the G7 and the fourth‑highest among advanced economies, pushing up debt interest spending further.

That said, lower‑than‑expected debt interest spending helps modestly improve the long‑term borrowing path, the OBR added.

General government borrowing and net debt in advanced economies

Source: IMF, OBR

Elsewhere, the OBR said unemployment is expected to rise to 5.3% this year – up from 4.9% in the November forecast – before falling to 4.9% in 2027.

Lindsay James, investment strategist at Quilter, said: “Reeves likes to say this Labour government is stimulating the economy but the reality is the forecast and actual results remain underwhelming at best.”

Indeed, the OBR admitted within its report that the fiscal outlook remains challenging – before even accounting for the geopolitical picture.

“And the tax burden remains high, demographic pressures are intensifying and the debt-to-GDP ratio could soar without a significant turnaround in fortunes,” James said.

Meanwhile, David Rees, head of global economics at Schroders, said Reeves’ Spring Statement amounted to little more than a refresh of the economic projections.

He noted that Schroders has factored in 0.5% of interest rate easing across both the upcoming March and May Bank of England meetings. However, Rees said “we remain concerned about underlying stickiness in services inflation”, as well as the potential for higher energy prices to squeeze real incomes and prevent rate cuts.

“Moreover, we are yet to be convinced that the UK’s rising unemployment rate is opening up genuine slack in the labour market that will result in significant declines in pay growth,” he added.

Take these figures with a pinch of salt

The escalating situation in the Middle East has raised questions about whether the OBR’s new forecasts were out of date before the report was even published.

On Saturday 28 February 2026, the US and Israel launched coordinated strikes on Iran – a move which has sharply intensified fears of a prolonged conflict, triggered a surge in oil prices and sent markets scrambling to reassess the outlook for inflation and interest rates.

Chris Beauchamp, chief market analyst at IG, said: “You have to wonder whether the chancellor has checked a data terminal recently, [as] today’s note that inflation is falling faster than expected is, like all plans, unlikely to survive first contact with the enemy.

“UK gas prices are rising at their fastest pace in recent history, and much faster than in 2022. The government might be optimistic but consumers are already beginning to fret.”

James agreed that the Spring Statement “already looks a little out of date”, noting that fiscal headroom may need recalculating in the weeks to come.

“Global shocks to the economic system have had outsized influence on the economy in the past – with another looming, it is unclear where the growth will come,” he added.

“As a result, markets are likely to give little heed to today’s announcements, focusing instead on the new reality we find ourselves in.”

Indeed, the OBR warned in its report that the picture it has painted is far from certain and is vulnerable to several major risks, with the conflict in the Middle East being the most immediate.

“Conflict in the Middle East, which escalated as we were finalising this document, could have very significant impacts on the global economy, particularly energy markets,” the OBR said.

Church said: “Geopolitical shocks also rarely arrive neatly. They tend to push governments into reactive choices – whether that means higher defence spending, fresh support to head off another inflation flare‑up, or renewed pressure to keep energy costs contained.”

She said there could be a subsequent “reshuffle” of Labour’s fiscal priorities, noting that the increase in fiscal headroom is the “one saving grace” which could provide some scope to help fund any reactive measures.

But war is not the only factor which may upset projections.

The OBR also pointed to broader global risks, including shifts in US tariffs, changes in global interest rates, uncertainty over productivity growth, future migration levels and a loosening labour market.

This is on top of the more structural pressures that come from an ageing population, elevated debt-servicing costs and the possibility of further shocks – whether geopolitical, economic or health-related – similar to those seen after the 2008 financial crisis, Covid-19 and the 2022 energy price spike.