Retail investors have overtaken wealth managers and are now the second-largest proportion of shareholders in investment trusts, according to a report by the Association of Investment Companies (AIC).

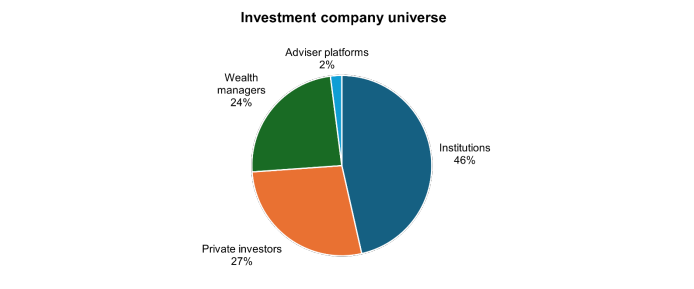

DIY investors who invest on platforms or through brokers now account for 27% of all shares issued by trusts, totalling some £57bn, while wealth managers own around £50bn worth of shares. Investors using popular platforms Hargreaves Lansdown, interactive investor (ii) and AJ Bell account for 16% of the total ownership base of investment companies alone, or £1 for every £6 invested.

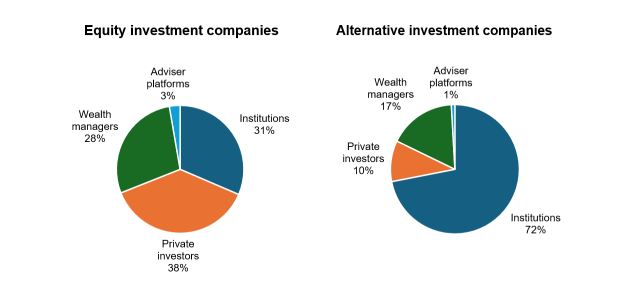

In particular, private investors dominate trusts investing in traditional equity asset classes, making this demographic the most influential here, with 38% (£40bn) of the shares in issuance. Institutions hold £40bn of equity trust shares, while wealth managers are third at £36bn. They have also taken a lead in flexible investments.

Source: AIC

Richard Stone, chief executive of the AIC, said there has been a “notable trend” in the rise of private investors who, in 2022, accounted for around £49bn worth of shares owned.

Conversely, wealth managers’ ownership has shrunk over the past three years, although he noted that “this trend may have run its course”.

This group consists of private client brokers and the wealth-management divisions of banks, as well as a small number of financial advisers who hold shares in their own nominee accounts.

“Between 2022 and 2024, wealth managers’ share of the investment company pie diminished from 27% to 24%, driven by a sharp fall in their ownership of alternative investment companies,” he said.

“However, in 2025 their holdings remained static at 24% and increased in value year-on-year from £49bn to £50bn. The partial resolution of the long-standing cost disclosure issue has increased confidence in the sector, though there is more work to do before we reach a satisfactory conclusion.”

The report looked at the ownership of £186.8bn worth of investment-trust shares, accounting for 90% of the total market capitalisation, with monetary figures estimated by multiplying these figures against the total market capitalisation.

It found institutional investors – including asset managers, pension funds and family offices – remain the largest investors in investment trusts, with £96bn worth of shares, while adviser platforms hold just £4bn. However, as a percentage, institutions’ ownership of trust shares dropped for the first time since 2022, dipping from 48% to 46%.

Where institutions dominate is the alternative assets space, with some 72% of shares owned (totalling £57bn). Wealth managers are a distant second (£13bn), while private investors only own 10%, or £8bn.

Source: AIC

This jumps to 81% of the private equity space, while they also own more than half the shares across property, infrastructure and debt trusts.

The only asset class where wealth managers own the most shares is the specialist trusts, with a 43% share. They hold the lion’s share of the Biotechnology & Healthcare and Technology & Technology Innovation sectors within this category, the report read.

Investment trusts remain popular, with assets excluding venture capital trusts (VCTs) rising to £259bn in the three year to the end of December 2025, up £2bn.

This is despite a steep reduction in the number of trusts available, with the universe dropping from 327 to 259 available investment companies. This means the average size for trusts has now passed the £1bn mark for the first time.

“We believe that investment companies have fundamental strengths that continue to make them attractive to a wide variety of investors, and the changes they have undergone since the end of 2022 have left them in an even stronger position to face the future,” said Stone.

Investment trusts: Not just a UK phenomenon

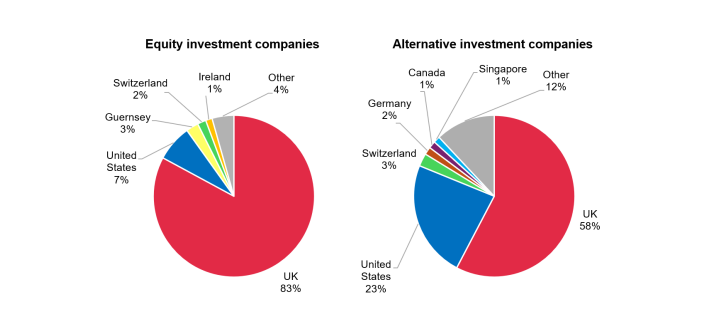

While the investment companies space is thought of predominantly as a UK-investor asset class (74% is owned by domestic investors, including UK-domiciled firms), there is appetite from other corners of the world.

Some 13% is owned by US stakeholders, with investors in Switzerland, Guernsey, Ireland and Canada also owning more than 1% of the total share issuance.

At a more minor level, Germany, Luxembourg, France, Singapore, the Netherlands, New Zealand, Norway and Japan make up the remaining 7%.

This changes when looking at the alternatives space, where UK investors own just 58% of the shares, while US investors account for 23% of the issuance.

Source: AIC

Who owns the most?

While institutions hold the most overall, the largest investor in trusts is wealth manager Rathbones, which holds some £10bn worth of shares. In second place, Evelyn Partners owns half this amount (£5bn).

In total, 10 firms hold more than £1bn of companies’ shares, including Brewin Dolphin, Quilter Cheviot, JM Finn and Canaccord Genuity Wealth.

At an institutional level, BlackRock Investment Management has the largest slug of trust shares, with £4bn invested in the sector, accounting for almost 2% of the entire industry.

European Clearing, which holds shares that are mid-transaction, is in second place, while Vanguard, City of London and Legal & General all own more than £2bn worth of trust shares, with a further eight fund groups topping more than £1bn.

Among retail investors, customers of Hargreaves (£14.5bn), ii (13.7bn) and AJ Bell (£5.1bn) are the top three owners of trusts, while investors using Charles Stanley, Columbia Threadneedle, Halifax Share Dealing, Fidelity and Barclays all own more than £1bn worth of shares.