Despite political pushback against environmental, social and governance (ESG) investing and tougher disclosure standards, several asset managers remain committed and continue to score strongly on sustainability.

MainStreet Partners’ 2026 iteration of the ‘ESG & Sustainability Barometer’ evaluates how effectively asset managers’ processes, resources and stewardship practices support sustainability outcomes, while also giving sustainable fund scores across key asset classes.

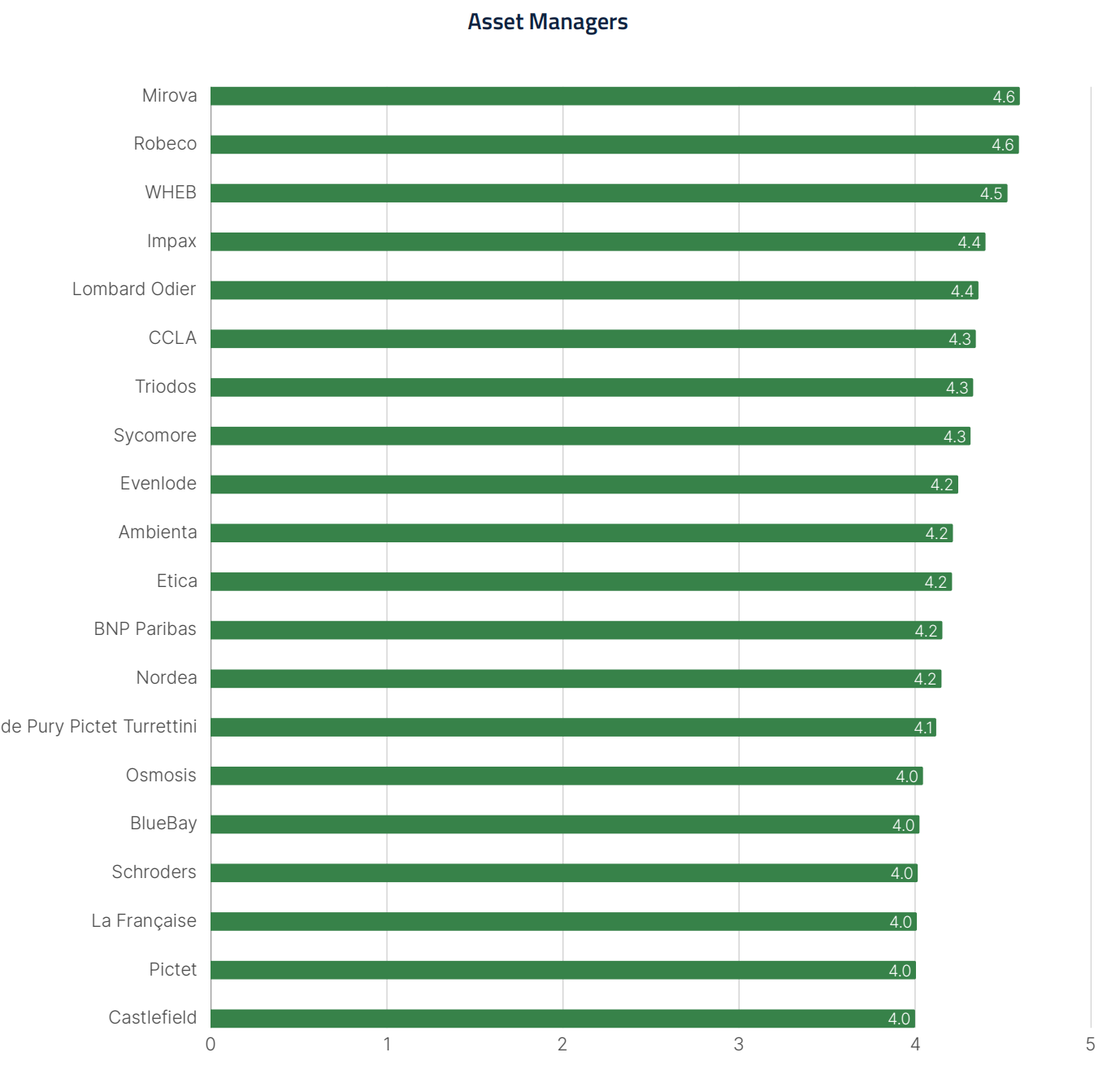

As shown in the table below, sustainability-focused boutique Mirova and mid-sized firm Robeco topped the rankings with scores of 4.6 out of 5.0. Larger houses such as Schroders (4.0) and BNP Paribas (4.2) also scored highly.

Source: MainStreet Partners

CCLA entered the top tier for the first time, with MainStreet Partners highlighting its engagement programme focused on real-world outcomes “rather than portfolio greening”.

Among managers with at least five sustainable funds assessed, Lombard Odier, Columbia Threadneedle and Robeco recorded the strongest average ratings for funds categorised as Article 8 under the EU’s Sustainable Finance Disclosure Regulation (SFDR). For Article 9 funds, leaders included Triodos, Sycomore and Mirova.

Article 9 funds must have a specific environmental and/or social objective, while Article 8 covers a broader set of funds claiming environmental and/or social characteristics.

However, MainStreet found that overall ratings drifted lower across all categories.

“This can be explained by rising sustainability standards and expectations across the industry, global asset managers facing divergent ESG requirements across regions with some scaling back commitments and MainStreet’s expanded coverage, which now includes a broader range of asset managers,” the report said.

Sustainable fund breakdown

The 2026 analysis draws on a universe of 1,600 ESG-labelled funds. When delving into performance across asset classes, MainStreet found that Article 9 equity strategies were led by European and global small- and mid-cap equity, which posted the highest average rating of 4.7.

“As many pure-play sustainable solutions and impact-oriented names within global equity funds tends to sit at the lower end of the market-cap spectrum, funds positioning themselves as impact or solutions-focused are typically concentrated in these areas,” the report said.

The weakest Article 9 cohort was global emerging markets equity, averaging just under 4.0, dragged down by inconsistent data and a more challenging operating environment.

Among Article 8 equity funds, global large-cap, thematic healthcare and European large-cap all clustered around the 3.5 to 3.6 score threshold.

“While healthcare may be perceived by some as an inherently sustainable theme, we adopt a broader perspective to ensure that the fund manager’s intentionality aligns with a genuinely sustainable approach and that potential negative outcomes are duly considered and mitigated,” MainStreet noted.

In contrast, long-short equity and East Asian equities logged a weaker average score of 3.3, reflecting data gaps and controversial exposures.

In fixed income, European and global bonds remained the strongest categories across both Article 8 and Article 9 funds, with respective average scores of 4.5 and 4.3. By contrast, Article 9 options remain scarce in the US, with the region’s 25 Article 8 funds averaging a score of 3.2.

SFDR overhaul incoming

However, the thresholds in which asset managers and their sustainable funds in Europe are categorised and assessed are set to change as regulators continue to crack down on greenwashing and look to improve transparency.

‘Greenwashing’ in funds refers to the practice of marketing investment products as environmentally friendly, sustainable or ESG compliant as a means of attracting capital – yet underlying holdings do not hold up against such claims.

Originally designed as a disclosure framework to curb greenwashing, the EU’s SFDR has evolved to become more of a de facto labelling system through its Article 8 and 9 categories.

It has been subject to criticism, teething issues and, ironically, increased risk of greenwashing since it first came into force in March 2021, with fund managers arguing that the regulation is overly complex, costly to implement and functionally flawed.

The European Securities and Marks Authority (ESMA) introduced ‘Naming Guidelines’ in May 2024 to provide clarity and curb exaggerated sustainability claims, requiring funds using ESG-related terms in their names to ensure at least 80% of holdings meet the ESG characteristics or sustainability objective implied.

Funds using more explicit terms such as ‘sustainable’ or ‘impact’ are further required to commit at least 50% of assets to be “invested meaningfully” in aligned sustainable investments.

Managers were given until 21 May 2025 to comply, which triggered a wave of rebranding. ESMA reported that around 1,500 funds – roughly 31% of those in scope – changed their names by December 2025.

Despite this, the MainStreet Partners report has found that greenwashing risk remains “material” in funds categorised as Article 8 or 9, with around 25% of Article 8 funds falling below the 3.0 out of 5.0 ‘ESG-assessed’ threshold and 30% of Article 9 funds below the 4.0 ‘sustainability-assessed’ bar.

In recognition of the ongoing challenges, European lawmakers have proposed a more radical overhaul of the SFDR regime, shifting to a labelling system more aligned with the UK’s Sustainability Disclosure Requirements (SDR) labels enforced by the Financial Conduct Authority in 2024.

The SFDR 2.0 proposal, published in November 2025, introduces three product categories.

The ‘transition’ category is for products where 70% of investments are in companies and/or projects that are not yet sustainable but have demonstrated a credible transition pathway or contribute towards improvements in wider themes, such as climate change.

The ‘sustainable’ category is for products ensuring at least 70% of investments are contributing to specific sustainability goals, meaning investments likely focus on companies and/or projects already meeting high sustainability standards.

The ‘ESG basics’ category is for products that integrate a variety of ESG investment approaches but do not meet the criteria of the ‘sustainable’ or ‘transition’ categories – i.e., it is more of a catch-all category.

According to the MainStreet report, 67% of existing funds would fall under ‘ESG Basics’, 19% under ‘transition’ and 14% under ‘sustainable’, which it said “indicates that most funds today are focused on meaningful ESG integration rather than explicit transition or sustainable objectives”.

The report added that SFDR 2.0 will ultimately set stricter standards and clearer expectations for the industry, presenting asset managers with an opportunity to strengthen transparency and realign products with genuine sustainability outcomes.

The SFDR 2.0 proposal also narrows the scope of who is directly impacted by the regulation, with portfolio managers and financial advisers no longer automatically included. However, if a portfolio manager is managing money on behalf of a fund that is in scope, they will have to follow the SFDR rules.