There is broad agreement among fund managers that Japan could be entering a transformative period but they remain focused on the fiscal and policy risks that will determine how durable momentum proves to be.

In February, Sanae Takaichi’s Liberal Democratic Party (LDP) enjoyed a landslide election victory, securing 316 out of 465 parliamentary seats – the largest share held by any party since 1945.

In response, the Nikkei 225 closed 3.9% higher and broke through the 57,000 barrier for the first time, as markets reacted positively to the prospect of smoother progress on reform and growth policies.

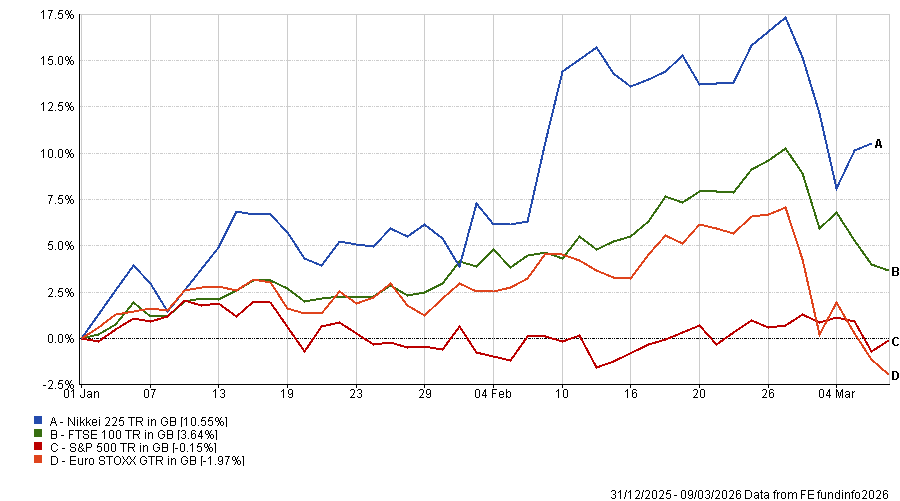

Performance of Nikkei 225 vs other major indices YTD

Source: FE Analytics

Takaichi has set out a pro-growth £99bn stimulus package, including large-scale public investment in strategic industries such as AI, defence and robotics.

In June, Japan’s Financial Services Agency (FSA) will also be announcing corporate governance code reforms in a bid to get companies to deploy excess cash and increase investment and share buybacks.

According to data by Asset Management One, Japanese companies – excluding financials – have average cash-to-assets ratios of 20.8%. In contrast, US and European businesses average 7.9% and 8.7% respectively.

David Aujla, multi-asset fund manager at Invesco, said he maintains a “constructive outlook” on Japanese equities and continues to view them as an important component of a well‑diversified global multi‑asset portfolio.

Aujla said Japan has increasingly drawn global investors looking beyond US mega‑cap AI names and argued that if the government maintains fiscal discipline alongside growth investment, it would reinforce existing structural reforms.

He added that much of this narrative is already well understood by markets, “so a period of consolidation in performance should not be ruled out”.

Gautam Samarth, multi-asset fund manager at M&G Investments, was more optimistic, saying valuations remain supportive and could improve further if reforms translate into stronger earnings.

James Bilson, global unconstrained fixed income strategist at Schroders, noted that the yen also now offers “an attractive opportunity” – supported by an improving growth outlook, the Bank of Japan’s likely further rate hikes and the potential for the fiscal risk premium priced into the currency to diminish if the government maintains its commitment to prudent policy.

Aujla was more cautious on the outlook for the yen, noting that “fiscal expansion can be a double-edged sword for a currency”.

“On one hand, currency markets typically favour economies with narrowing budget deficits over those with widening ones, which could point to further yen weakness but, on the other hand, investors tend to reward currencies associated with accelerating economic growth relative to peers,” he said.

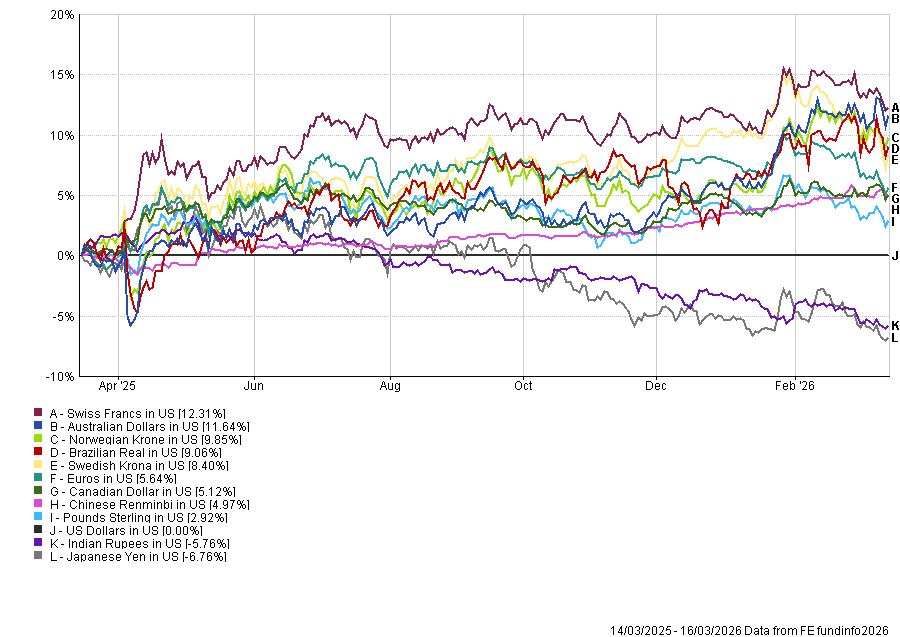

Although the yen did experience a brief post-election bounce, it has been the weakest major currency against the US dollar over the past year.

Performance of currencies vs the dollar over 12 months

Source: FE Analytics

“Looking further back, the longer‑term trend remains decidedly negative, with the yen depreciating by nearly 50% versus the US dollar over the past 14 years,” said Aujla.

However, he noted that “given its already depressed starting point, it would not take a dramatic shift in sentiment for the yen to reprice meaningfully should a more constructive narrative take hold”.

But there are wider concerns that Takaichi’s pro-growth agenda poses risk. Steve Ryder, senior portfolio manager at Aviva Investors, said the growth-friendly policies are “offset by proposals like suspending the consumption tax, which have unsettled markets because of the implied strain on public finances”.

To tackle the cost-of-living crisis in Japan, Takaichi pledged to impose a temporary two-year suspension of the 8% consumption tax on food and non-alcoholic beverages – a policy that would remove around 6% of total annual tax income.

Investors baulked at the lack of clarity over how the country – which has the highest debt burden in the developed world at 230% to GDP – would fund this proposal. After Takaichi’s victory, two-year Japanese government bond (JGB) yields jumped to their highest level in decades, while the 10- and 30-year yields moved up toward roughly 2.3% and 3.6% respectively. These have since eased back slightly.

In her post-election victory speech, Takaichi reiterated her intention to avoid issuing bonds to fund the tax suspension and to instead seek other revenue streams or savings.

As such, Alberto Talero Garcia, global rates portfolio manager at JP Morgan Asset Management, said he sees reduced risk of a large near-term fiscal expansion that would be financed by debt.

“The government’s tone on potential consumption tax cuts has been cautious, and Japan’s deficit position remains comparatively healthy, together pointing to a more measured fiscal stance than markets feared prior to the event,” he said.

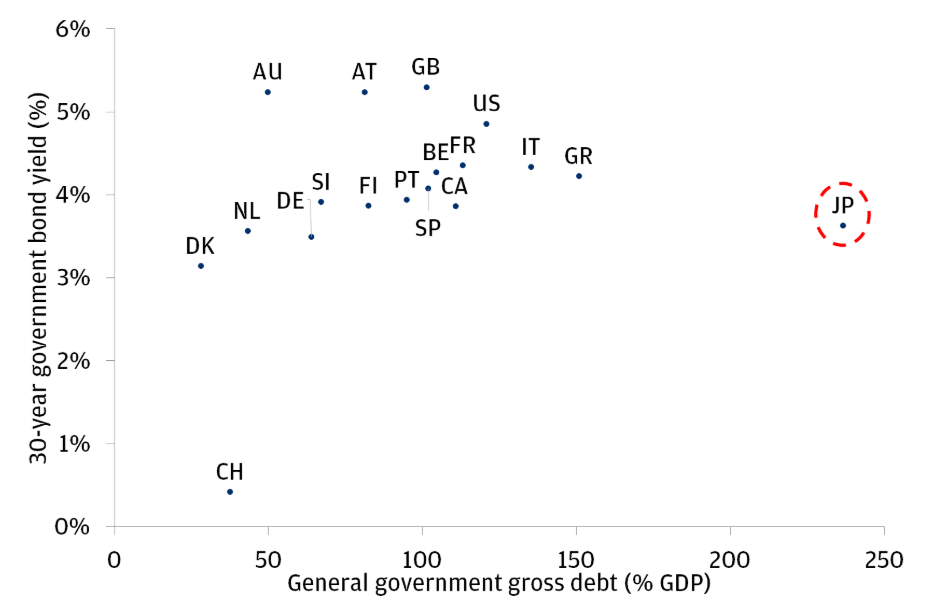

Even without more debt issuance, the country is already spending a quarter of its budget on interest, according to JP Morgan. This is despite Japanese government bonds typically trading at a similar yield to economies with stronger fiscal fundamentals.

30-year government bond yield (%) vs general government gross debt (% GDP)

Source: JP Morgan, International Monetary Fund, Bloomberg. Data as of 2024 for debt figures, January 2026 for government yields.

However, Samarth pointed out that Japan is also “one of the few major Western economies where the debt-to-GDP ratio has declined in recent years”.

“This trend can continue even if the primary deficit widens and it could accelerate if the growth and reform measures pursued by Takaichi prove effective,” he said.

Samarth said he has not made any portfolio adjustments since Takaichi’s election, “but several of our strategies took advantage of the yield sell-off in January to build positions in long-dated Japanese government bonds, complementing our long-standing equity exposures”.

“We believe the rise in long-end JGB yields presents compelling value and we have a preference for 30-year JGBs,” he said.

Although Aujla said Japanese government bond yields appear attractive at present, he is leaning toward caution.

“Until there is greater clarity on the fiscal package, concerns are likely to persist that more proactive, reflation‑oriented fiscal spending could heighten both fiscal and inflationary risks, potentially pushing yields even higher, bearing in mind that rising yields imply falling bond prices,” he said.

“In our portfolios, we have no direct exposure to JGBs, though indirectly may gain exposure through some of the active fixed income managers and index funds we allocate to.”