Europe burst back into life in 2025 as enthusiasm for defence stocks encouraged new money into the region. The MSCI Europe ex UK index rose 26.2% last year, helped in part by investors beginning to question the long dominance of US equities.

The market has dropped back this year, down 0.3%, as investors worried over a prolonged war in the Middle East between the US and Iran. The closure of the Strait of Hormuz has left many concerned about the economic implications for Europe, with the narrow waterway pivotal for oil, gas and other major commodity transportation.

Yet a quick end to the conflict, as US president Donald Trump initially alluded to, could return Europe to the top of the rankings again in 2026.

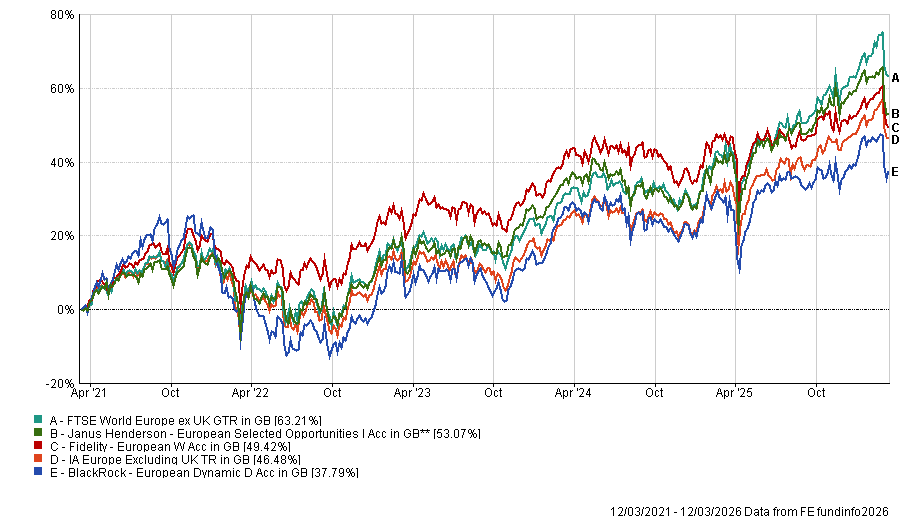

For those interested in investing on the continent, three funds dominate the active European equity landscape: BlackRock European Dynamic (£5bn), Fidelity European (£3.7bn) and Janus Henderson European Selected Opportunities (£1.6bn).

All three sit in the IA Europe Excluding UK sector and carry similar ongoing charges of around 0.9% but are built differently, behave differently and reward different kinds of investors.

The three philosophies

The most straightforward of the three is Fidelity European, managed by Samuel Morse and deputy Marcel Stotzel. Darius McDermott, managing director at FundCalibre, described it as taking “a disciplined, cautious, long-term approach” focused on companies capable of sustainably growing their dividends.

Although it is not an income fund, that dividend discipline gives it a quality-income character that makes it “attractive for investors seeking a rising income stream”.

Rob Morgan, chief analyst at Charles Stanley Direct, called it “a less style-orientated fund and a valid alternative as a core holding in the sector”.

Janus Henderson European Selected Opportunities, co-managed by Marc Schartz and Robert Schramm-Fuchs, is the oldest of the group, having launched in 1984. McDermott said it “runs a flexible, blended style, tilting between growth and value depending on the prevailing market environment, which can be valuable in more volatile periods”.

BlackRock European Dynamic is the highest conviction of the three. Managed by Giles Rothbarth, it has a quality-growth tilt that has weighed on returns in recent years.

Morgan said the team “take a flexible, concentrated approach and is one of the most capable and well-resourced in the sector” but noted that “given the high-conviction nature of the strategy and willingness to be very differently positioned from the index, underperformance over some periods shouldn't be considered unusual”.

Performance of funds against index and sector over 5yrs

Source: FE Analytics

Where the funds differ

BlackRock has the heaviest weighting to industrials at 31.8% and telecom, media and technology at 16.7%, reflecting its quality-growth tilt. Fidelity has the highest allocation to consumer products at 17.5% and basic materials at 10.8%, which gives it a more cyclical texture. Janus Henderson sits between them, with the highest healthcare weighting at 15.9%.

McDermott said that BlackRock's recent underperformance is in some ways the most interesting part of the story today. “Many of its holdings have seen earnings upgrades that simply haven't been reflected in share prices, so on a risk-reward basis it arguably offers the most upside,” he said, though he added that choosing one of the three was “a close call”.

The broader outlook

Morgan acknowledged that the outlook is “uncertain” but pointed to a structural feature of the market that often goes unnoticed: roughly two-thirds of corporate sales and profits from European listed companies now come from outside Europe.

The near-term catalyst Morgan and others point to is Germany. Berlin's decision to relax its constitutional debt brake should translate into higher spending on defence and infrastructure – a meaningful shift for an economy that has spent years dragging on European growth.

McDermott was direct about the risk of dismissing the region. “Europe is often talked down as a region, yet it consistently produces high-quality, cash-generative companies,” he said, arguing that the gap between business fundamentals and investor sentiment continues to create opportunity for long-term investors.

Glenn Meyer, head of managed funds at R C Brown, was more cautious.

“Europe is potentially caught in the crosshairs of geopolitical change,” he said, noting that politics and markets do not move in tandem – and that timing any reallocation is essentially impossible.

Then there’s cheapness. European equities trade at a substantial discount to US peers on most measures and Morgan said that “building more resilience into portfolios generally means diversifying across geographies, styles and asset classes”.

“Europe is a major consideration given the difference in valuations when compared with the US,” he said.

The verdict

Morgan's pick among the three was BlackRock European Dynamic, with the caveat that its quality-growth tilt demands patience. For investors who want a cleaner core holding, he pointed to Fidelity European as “a valid alternative”.

McDermott leaned toward BlackRock on risk-reward grounds, calling it the most interesting of the three at this point in the cycle, while acknowledging the call was close.

Meyer declined to single out any of the three, preferring instead to advocate for diversification across styles, market capitalisations and geographies rather than concentration in any single strategy. “I think I might do better with a range of management styles and market cap exposures,” he said.

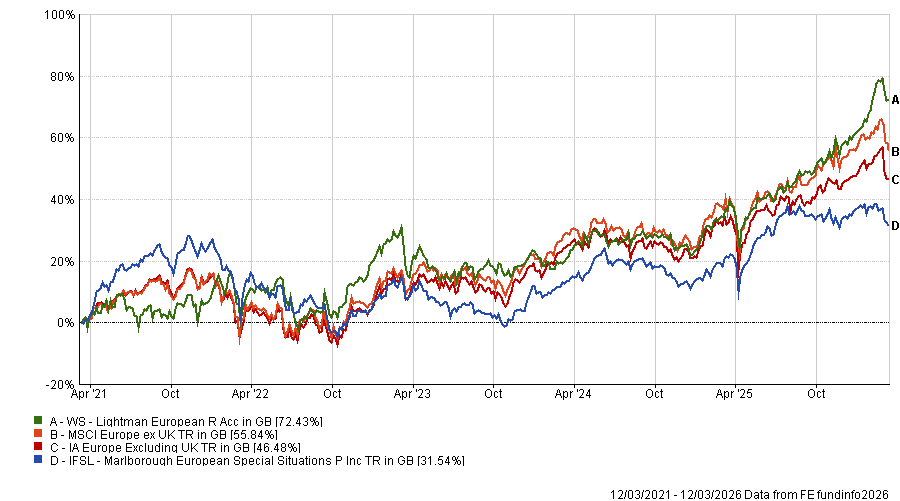

For those willing to look beyond the three, McDermott highlighted IFSL Marlborough European Special Situations, managed by David Walton and the Hargreave Hale team, as a way of accessing “the most underappreciated growth stories in Europe” through smaller companies.

Finally, Morgan suggested WS Lightman European, run by Rob Burnett, as a value-oriented complement to BlackRock European Dynamic for investors who want to hedge their style exposure.

Performance of funds against index and sector over 5yrs

Source: FE Analytics