Running your winners sounds like a sensible approach in theory, but investors are better off getting out when a stock achieves a fair value, according to Schroders’ Simon Adler.

The head of value equities said the idea of letting your winners run despite a rising price-to-earnings multiple “sounds great” but noted there is strong evidence to sell long before a company is deemed expensive.

He said: “Running your winners sounds lovely, it’s a beautiful story. When you do it well, everyone thinks you’re a genius. But when you do it and it falls 50% afterwards, how does it feel then?”

On his £1bn Schroder Global Recovery fund, Adler and his team have a strict policy to sell when a stock hits their ‘fair value’ figure, which is different depending on the company and determined with reference to normalised profitability (the average profit a stock makes over a full economic cycle). It is then analysed versus a risk score.

To assess strengths and weaknesses, the team uses a database looking at all the stocks the fund has bought over the years, spanning more than a decade.

It tracks what was deemed a ‘fair value’ for the company at the time and logs the performance of the stocks sold, as well as those that were brought in to replace the outgoing companies.

“When we sell a stock, it goes up a little bit more on average, but what we buy goes up by more,” said Adler.

Selling is one of the part of the equation, the other is making sure that they pick the right stocks to bring into the portfolio.

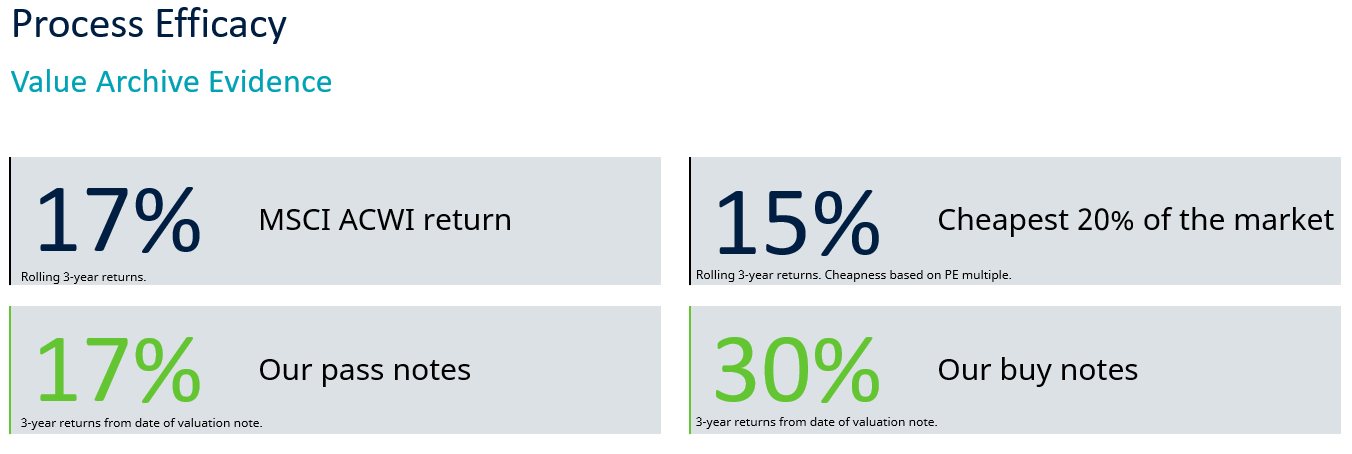

Over the past 10 years, the team has an enviable track record, according to its own data. The stocks that the team passed up on the opportunity to buy averaged a return of 17% three years later. By contrast, the stocks it bought averaged a three-year return of 30%, almost double.

Source: Schroders

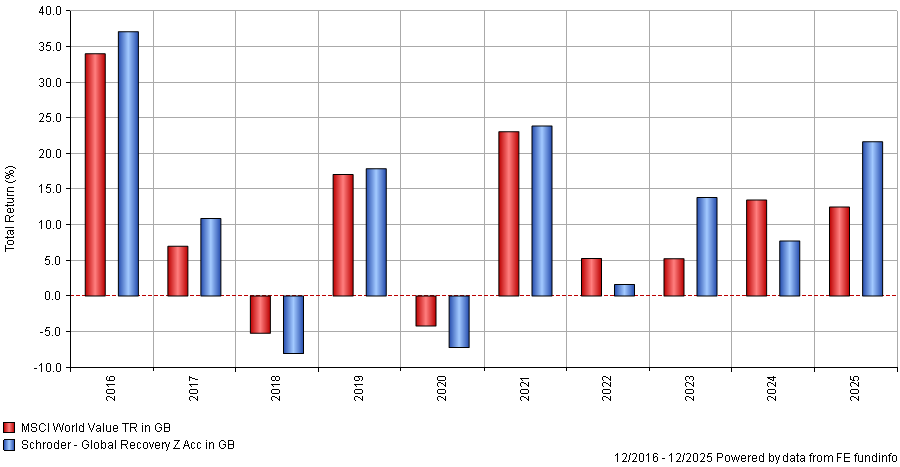

This is also backed up by the table below, which shows Schroder Global Recovery has beaten the MSCI World Value index in six of the past 10 calendar years. It is also on track to do so again in 2026.

Performance of fund vs MSCI World Value index over 10yrs

Source: FE Analytics

Once it has its stock selections in place, the team then aims to enhance this further with portfolio construction. Companies with lower risk scores are allocated larger positions, although the range of the largest and smallest stocks is kept relatively narrow. Diversification is also a key factor.

“We will build the most diversified portfolio we can within the cheapest absolute part of the market,” Adler said, although the managers will “never diversify at the expense of absolute valuation”.

His fund has a strong track record of doing this as it currently a top-quartile performer in the IA Global sector over one, three and five years. It is in the second quartile over the past decade – the first half of which was challenging for value funds like Schroder Global Recovery because of low inflation and low interest rates.

Its outperformance is despite being unable to own some of the more expensive stocks in the market, such as the Magnificent Seven, which have thrived in recent years. But Adler has learned not to worry if he cannot own something.

The closest he has come to owning one of the Magnificent Seven stocks in recent years was Meta, when its valuation more than halved in 2023. Despite such a steep fall, “it didn’t quite get cheap enough”, said Adler.

However, almost everything eventually lands in his value bucket at some stage. For example, he noted that five years ago consumer goods companies (which had steadily performed brilliantly in the 2010s) were on 30x earnings. He bought the same companies recently at 10x.

“Five years ago, luxury was the most highly valued stuff on the planet, more or less. A year ago we were buying it on incredibly attractive valuations. That is a great example of how expensive stuff has become cheap,” he said.

In 2020 he was buying banks, which were “on half book”. “Now we can sell them on 2x book,” he said.

The key is patience. When discussing all of the above, the fund manager reiterated the word “wait” four times – whether it be waiting for stocks to become cheap or waiting for them to turn things around and become appreciated by the market.

Most recently, there has been a sell-off in software companies, which have fallen out of favour as investors price in a world where AI can take over the technology landscape.

They have fallen dramatically, but Adler noted that “valuations are nowhere near where we need them to be” to be worth buying.

“That’s fine. I’ll just wait and if they come on the screen, then we’ll do the work then.”

Investors would be wrong, however, if they thought the fund was devoid of technology names.

“We own some tech stocks but they are old tech, whether they make printers or PCs. We’re not going to look at the Magnificent Seven. But at some point in the next 10 years there is a decent chance that we will buy them: they will just be on 10x earnings, not 30x,” he concluded.