AI, digital connectivity, automation and cloud computing are driving exponential growth in data creation, storage and processing. While much has been made of the investment potential – and risks – of investing in companies linked to the new digital economy, it is worth noting that the data associated with this is not intangible.

Behind every AI query lies a vast physical infrastructure that consumes energy, materials and capital at scale. As data volumes surge, so too does the energy intensity of the digital economy. This creates powerful investment opportunities across infrastructure and the supply chains that enable it.

The rapid adoption of AI is fundamentally more energy-intensive than previous waves of digitalisation. AI workloads rely heavily on graphics processing units (GPUs) rather than traditional central processing units (CPUs). GPUs consume three-to-four times more power than CPUs.

Their widespread deployment is expected to add significantly to total global power demand by 2030. Even simple actions illustrate the shift: an AI-based search query can consume considerably more electricity than a standard internet search.

At the core of this shift are data centres – the physical backbone of the digital economy. Today, they account for around 5% of total US electricity consumption. That figure is expected to rise to 11-12% by the start of the next decade as demand accelerates, requiring over $500bn of investment in data-centre infrastructure alone. Europe is following a similar trajectory.

As digital systems become more autonomous and connected, data intensity will increase further. Autonomous vehicles, for example, can generate up to 40 terabytes of raw data per hour from cameras, radar and sensors – the equivalent of hundreds of billions of emails or thousands of hours of continuous smartphone use.

Meeting this surge in data and computing demand requires a significant expansion of the global energy system. After years of stagnation, electricity demand is accelerating across global markets, with renewable sources of energy very much in the vanguard.

These are no longer a simple substitute for fossil-fuel generation – they are becoming an essential source of incremental capacity. IEA analysis shows that renewables are set to dominate new global power‑generation capacity additions through 2030, while long‑term scenarios imply multi‑trillion‑dollar investment requirements this decade to expand clean generation and supporting infrastructure.

With recent disruptions to oil and gas supplies placing energy security front and centre of national debate, the role of renewables can only become more important.

At the same time, electricity grids must be expanded and modernised to cope with higher loads, increased intermittency and the geographic concentration of data centres. Transmission, distribution, energy storage and grid resilience all become critical enablers of the digital economy.

Despite record renewable deployment, more than 80% of global energy demand is still met by fossil fuels, while overall energy consumption continues to rise. That combination highlights both the scale and longevity of the investment opportunity created by the data-driven energy transition.

For investors, this backdrop presents compelling investment opportunities within the critical minerals sector, the building blocks of modern energy systems.

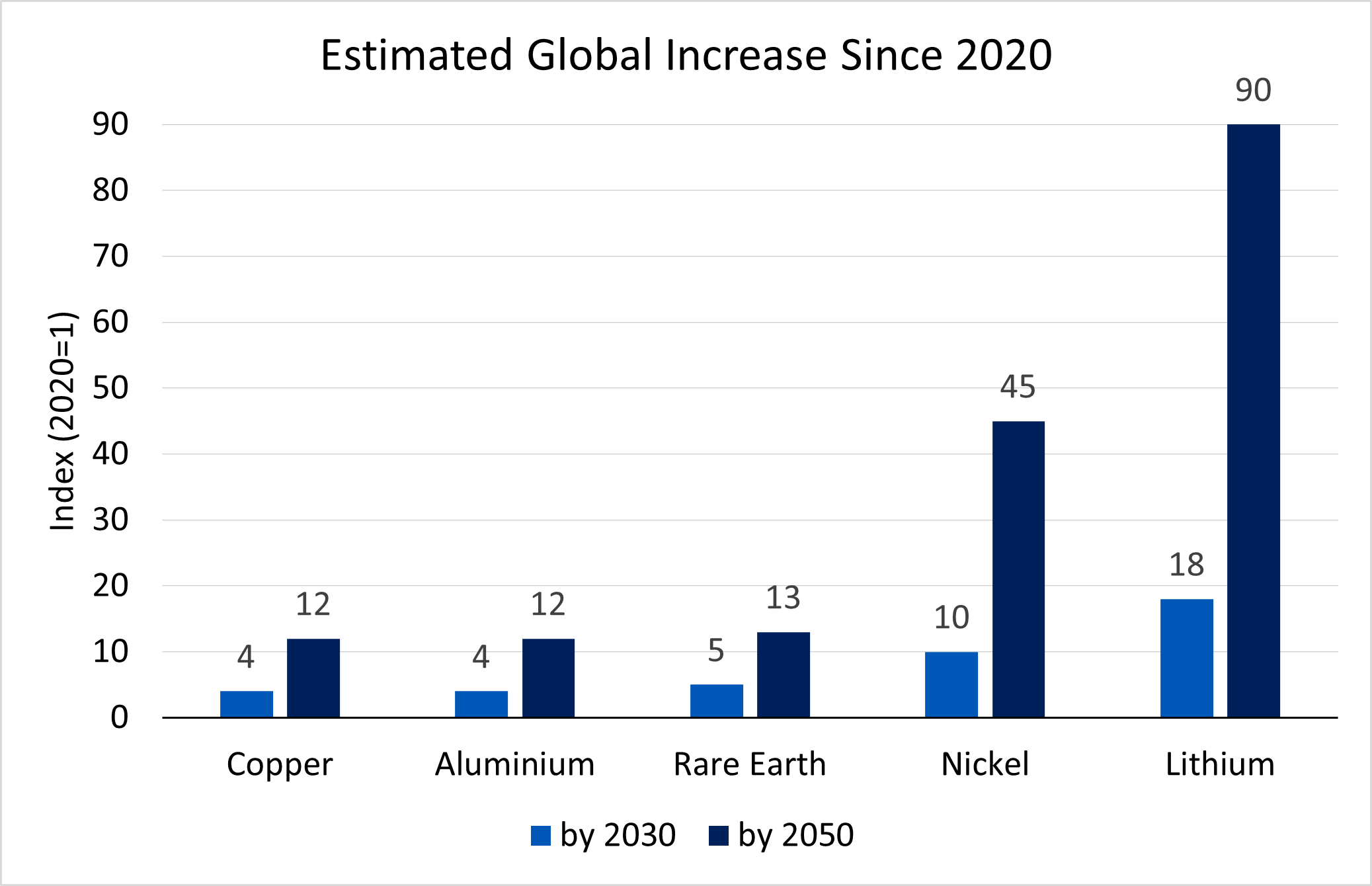

This electrification and digitalisation of the global economy is creating huge demand for raw materials. Copper is essential for power transmission and data-centre connectivity, while aluminium underpins lightweight infrastructure. Lithium and nickel support energy storage and grid resilience.

Source: Supply chain analysis and material demand forecast in strategic technologies and sectors in the EU – A foresight European Commission study 2023. Forecasts are not guaranteed and actual events or may differ materially.

As AI and data growth push electricity demand higher, they also drive demand for the critical minerals required to build, connect and power the system.

These demand drivers are structural, long-term and underpinned by multiple megatrends, with geopolitical tensions and increased competition for scarce resources adding a further dynamic.

Importantly, decades of underinvestment in miners operating within the sector and the lead time required to bring new mines fully online have exacerbated this supply/demand imbalance.

Within the abrdn Future Raw Materials ETF, we target exposure to companies positioned along these supply chains, capturing the upstream beneficiaries of the data-driven energy transition, which we believe can be a significant driver of portfolio returns.

A primary focus is therefore on the extraction and processing of those minerals that present the most compelling supply/demand imbalances against this broader market backdrop.

Copper underpins everything from data‑centre wiring to grid expansion, making it one of the most important materials supporting our fast-expanding digital world. An example of a company in this space is Capstone Copper, a rapidly growing copper producer.

Most of Capstone’s production is based in the US, Mexico and Chile, with several projects expected to drive meaningful production growth over the coming years.

SQM (Sociedad Química y Minera de Chile S.A.) is a leading producer of lithium, a critical input for batteries and energy storage. Lithium plays a vital role in storing power and improving the resilience of electricity systems.

The company benefits from access to high-quality, low-cost resources and a pipeline of projects aligned with long-term growth in lithium demand.

Finally, as electricity systems come under increasing strain, nuclear offers a stable, low-carbon source of baseload power. Cameco Corp, a Canada‑based nuclear fuel and uranium producer is a prime example within this theme. Companies such as Cameco represent an important part of balancing the digital-economy energy equation.

Data may be digital, but its value is realised in the physical world. Just as gold needs miners and machinery, data depends on power, infrastructure and critical minerals. For investors, this creates tangible, long-term investment opportunities beyond the technology headlines.

David Clancy is portfolio manager of the abrdn Future Raw Materials ETF. The views expressed above should not be taken as investment advice.