The 2026 Iran conflict has delivered one of the biggest macro shocks to global investor confidence in years, with fund managers pulling back from stocks and expecting the economy to go into stagflation, a closely watched positioning survey shows.

Operation Epic Fury, the joint US-Israeli military campaign launched on 28 February 2026, opened with nearly 900 airstrikes in the first 12 hours, killing Iranian supreme leader Ali Khamenei and targeting nuclear sites and military infrastructure. Iran retaliated with missiles and drones across the region, closing the Strait of Hormuz, through which roughly 20-30% of global oil, gas and fertiliser shipments normally pass.

The IEA described the resulting supply disruption as the largest in the history of the global oil market. Global equities fell sharply, bond markets sold off as rate cut expectations evaporated and shipping costs spiked as tankers rerouted away from the Gulf. A temporary truce was announced in early April, but Iran has rejected a US peace plan and the conflict remains unresolved.

BofA’s April Global Fund Manager Survey, covering 170 respondents managing $511bn in assets, found that asset allocators have darkened in their economic outlook, rapidly repriced risk and repositioning portfolios because of the conflict.

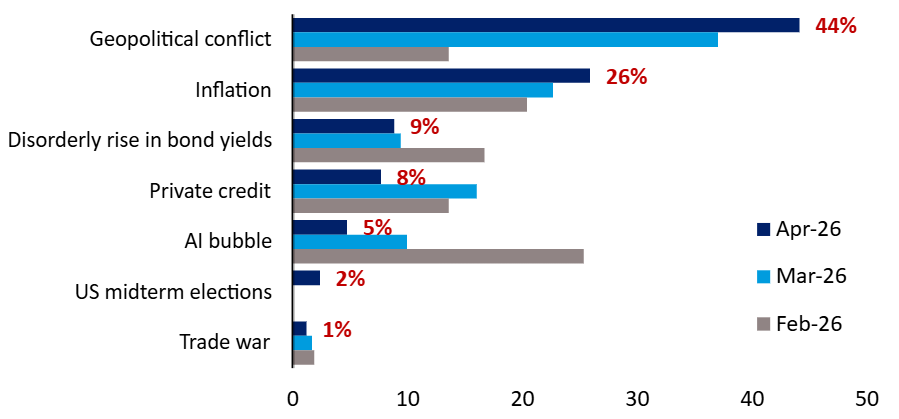

What fund managers consider the biggest ‘tail risk’

Source: BofA Global Fund Manager Survey, April 2026

Unsurprisingly, geopolitical conflict has topped the tail risk rankings for two consecutive months, cited by 44% of respondents in April. This is up from 14% in February and 37% in March. Inflation, linked to higher energy and food costs caused by the closure of the Strait of Hormuz, is the second largest tail risk.

The number of fund managers worried by a disorderly rise in bond yields, strains in private credit and a potential AI bubble has declined in recent months as Iran dominated the headlines and market activity.

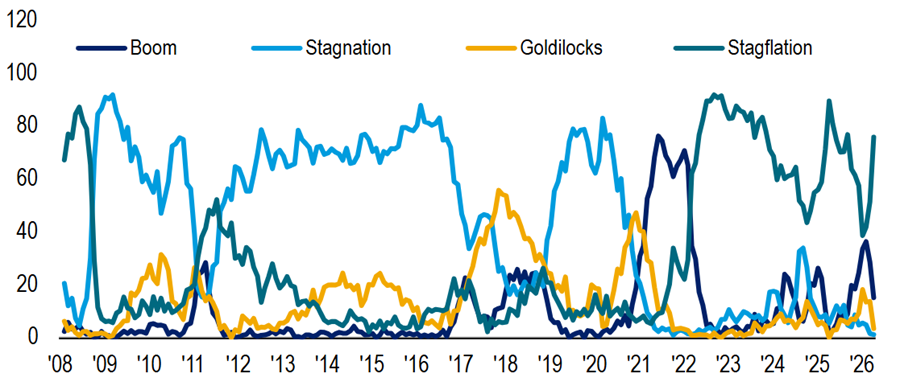

Fund managers’ expectations for the global economy over the next 12 months

Source: BofA Global Fund Manager Survey, April 2026

Expectations of stagflation, defined as below-trend growth combined with above-trend inflation, have surged from 51% to 76% of respondents in a single month. Stagflation is widely seen as one of the worst environments for risk assets.

The boom scenario, which assumed above-trend growth alongside elevated inflation, more than halved from 29% to 15%, while ‘goldilocks’, the benign backdrop, has nearly disappeared, falling from 14% to just 4%. However, just 1% forecast stagnation, or below-trend growth and inflation.

The oil price shock is a key part of this. Investors now forecast Brent crude at $84 per barrel by year-end 2026, a 38% increase from $61 at the start of the year. Some 28% of respondents expect $90 or above, up sharply from 12% a month ago.

Inflation expectations have surged as a result: a net 69% of investors think inflation will be higher in 12 months’ time, up from 45% last month and the highest since May 2021. On growth, a net 36% expect a weaker economy – compared with last month’s net 7% thinking it would strengthen.

Global fund managers’ sentiment (growth expectations, cash level and equity allocation)

Source: BofA Global Fund Manager Survey, April 2026

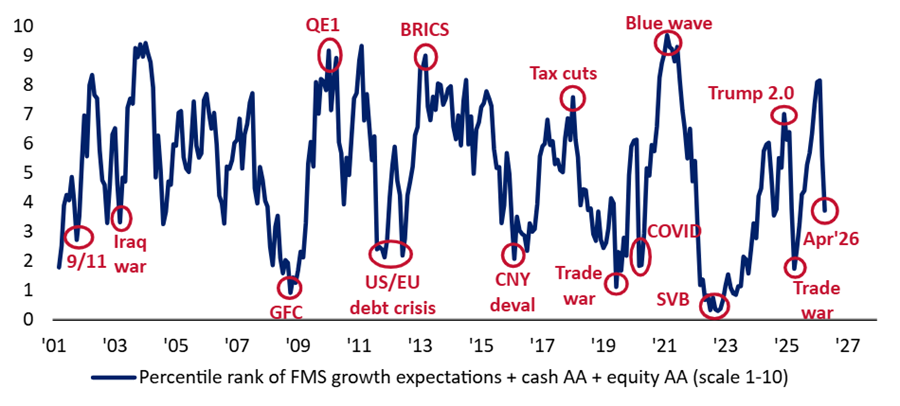

Sentiment among asset allocators has collapsed as a result. BofA’s composite sentiment indicator, which draws on cash levels, equity allocation, and growth expectations, dropped to 3.7 from 5.6, the lowest reading since June 2025.

It is worth noting that current reading sits well above recent extremes. The indicator reached 1.7 during the April 2025 tariff tantrum, 1.6 at the October 2023 S&P low and 0.3 during the October 2022 UK pension crisis.

The risk aversion appears in behaviour as well as sentiment. A net 24% of investors are now taking lower than normal risk levels, compared with 14% last month.

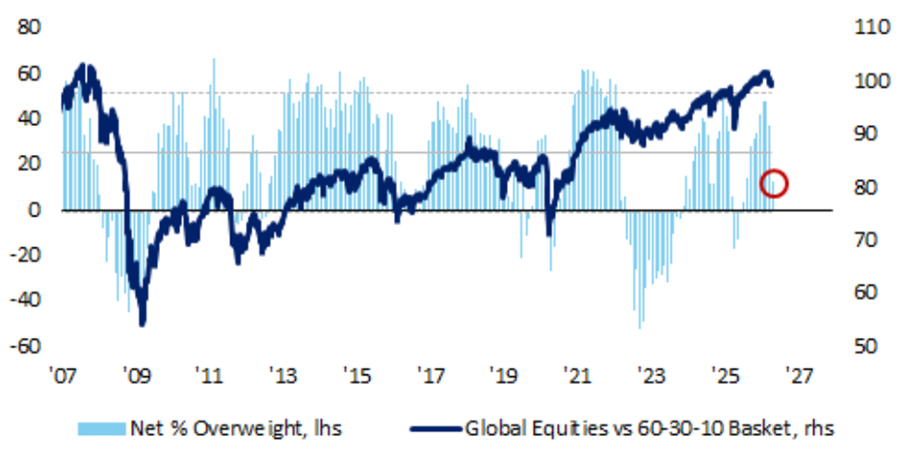

Net % overweight equities & global equities vs 60/30/10 basket

Source: BofA Global Fund Manager Survey, April 2026

Fund managers’ equity allocation has fallen sharply to net 13% overweight from 37% last month, the lowest reading since July 2025.

BofA’s strategists pointed out that recent lows include a net 17% underweight during the April 2025 tariff tantrum and net 52% underweight in September 2022, suggesting there is considerable room for further rotation out of stocks if conditions worsen.

Despite the pullback, net 64% of investors still regard US equities as overvalued, though that reading has fallen to its lowest since February 2019. More pressingly, investors now thinking global corporate profits will deteriorate for the first time since September 2025, with a net 14% expecting this compared with a net 44% expecting them to grow in January 2026.

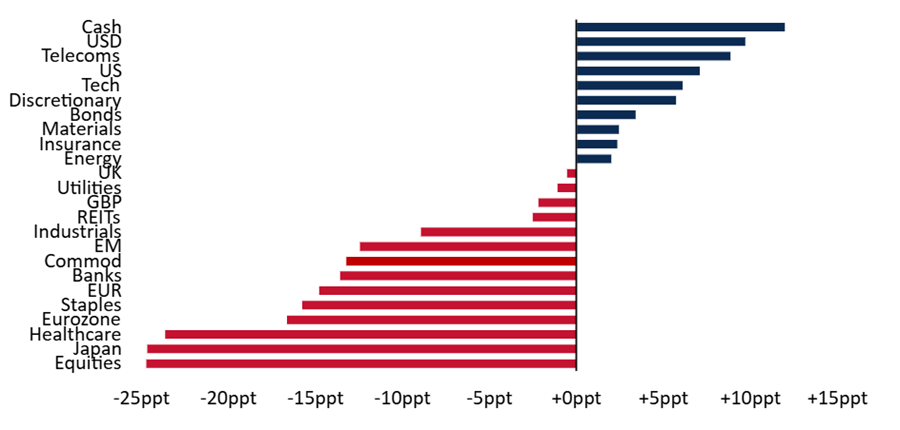

Monthly change in fund managers’ positioning

Source: BofA Global Fund Manager Survey, April 2026

Over the past month, managers have increased allocations to cash, the US dollar and telecoms while cutting equities in general, Japan and healthcare.

The Japan move stands out as investors flipped from net 14% overweight to net 11% underweight in a single month, the first significant underweight since November 2024.

A net 20% of investors are overweight cash, up from 8%. Technology allocations increased to net 14% overweight from 7%. Emerging markets remain deeply held at net 41% overweight, down from 53% last month.