US valuations continue to make the market expensive, despite the recent pullback following the start of the Iran war, according to Hetal Mehta, chief economist at St. James’s Place (SJP).

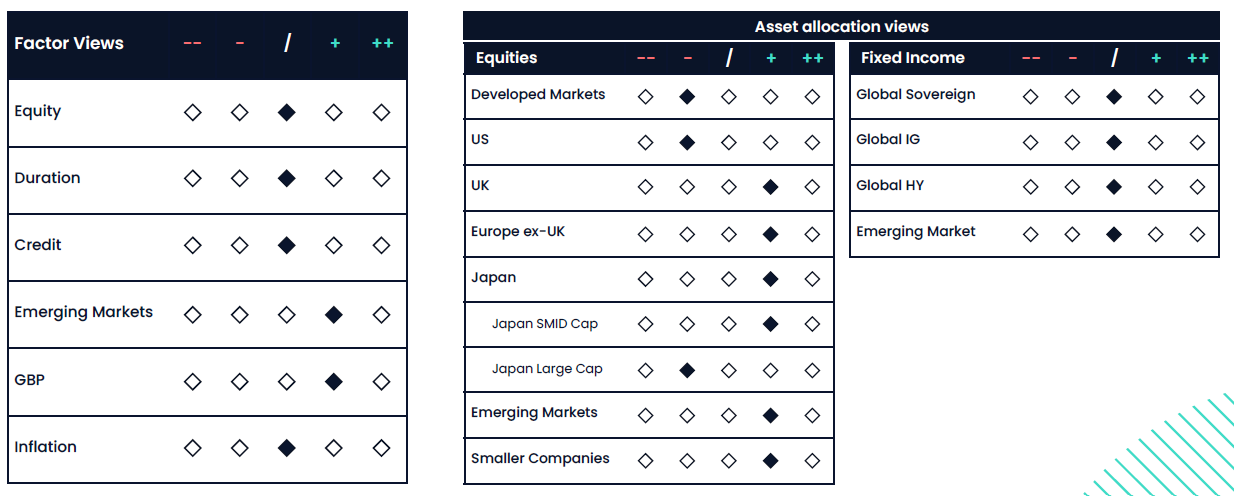

As a result, the firm remains underweight the American market, preferring the UK, Europe, Japan and emerging markets.

“Our preference for equity markets outside the US remains unchanged. Despite the recent pullback, US valuations continue to look elevated – both relative to other regions and compared with its own history,” he said, adding that the concentration in ‘Magnificent Seven’ stocks creates additional diversification problems.

This is in contrast to BlackRock, the world’s largest asset manager, which last week returned to an overweight position in US equities, having previously taken a neutral position at the beginning of the war.

Mehta noted that the investment team looks at the world through the lens of valuations, fundamentals and sentiment. With this in mind, he said some of the markets that have re-rated the most since the start of the Middle East crisis (namely Europe and parts of Asia) remain more compelling.

Source: SJP

The UK remains “relatively defensive” thanks to its high exposure to the energy sector, which has performed exceptionally well as energy prices have risen.

“Rising investment in defence companies, reflecting heightened geopolitical risks, could provide an additional tailwind and UK valuations also remain attractively discounted compared with global markets,” said Mehta.

European equities outside the UK have a “balanced mix” of value and growth alongside steady profitability.

“Although Europe is closer to the conflict and relies on some of the affected resources, many of its listed companies generate earnings globally, which helps to reduce the impact of local disruptions on their equity returns,” he added.

Turning east, Japan is perhaps where the wealth manager is finding the “strongest opportunities”, as ongoing corporate reforms and additional fiscal support from the government are improving the outlook.

“Valuations are attractive and profitability is robust. Smaller and mid-sized companies in Japan look particularly promising as their domestic earnings focus makes them less exposed to external pressures, offering valuable diversification,” said Mehta.

Meanwhile, emerging markets (which are dominated by Asian powerhouses China and India but also span Latin America and some eastern European and African countries) “also offer attractive valuations and good diversification benefits”.

“With a growing emphasis on domestic demand rather than export-led growth, earnings in these markets appear more resilient,” said Mehta.

Overall, the firm is neutral on equities, with the chief economist noting that fundamentals remain stable, with “profitability and margins still above long-term median levels”, although he admitted there is a risk that the Iran conflict could “precipitate earnings revisions”.

In the bond space, the firm is neutral across all areas of fixed income, with the chief economist noting that falls in government and corporate bond prices have improved valuations and therefore made yields more attractive.

“Government bonds provide a valuable cushion against global growth risks. Given the uncertain inflation backdrop linked to the conflict, inflation-linked bonds continue to provide a helpful hedge alongside equity exposure,” he said.

Last quarter, SJP added exposure to US treasuries and other sovereign bonds while trimming some investment-grade credit. It also introduced an emerging market debt allocation, which Mehta said is “an important and underrepresented area of global bond markets that provides meaningful diversification”.

For now, this neutral positioning reflects the uncertainty surrounding markets. While the ongoing conflict in the Middle East could create economic pressures, he said the severity and duration of the impacts of the war are unknown.

The blockage of the Strait of Hormuz has led to supply disruptions in oil, but the uncertainty surrounding the conflict is creating wider ripple effects across global supply chains, said Mehta.

“If the disruptions persist or intensify, the economic impact is likely to become more prolonged, although a ceasefire in the coming months could point to a more contained scenario with limited impacts,” he said.

As such, the team has increased the likelihood of a mild stagflation scenario from 10% to 15% and reduced the chance of a stronger pick-up in growth by 5%.

However, SJP’s base case remains that the world will stay in a ‘steady state’, an outcome with a 55% probability.

“While risks have tilted a little more to the downside, the adjustments are small,” he said.