China remains one of the most divisive markets in global investing. For some, decades of economic expansion have not translated into shareholder returns, raising questions about the investability of the market itself. For others, the combination of policy direction and private sector innovation continues to create a fertile, if selective, opportunity set.

Sid Jain, deputy manager of the GQG Partners Global Equity fund, sits in the sceptical camp, arguing that the market’s growth has not accrued to investors.

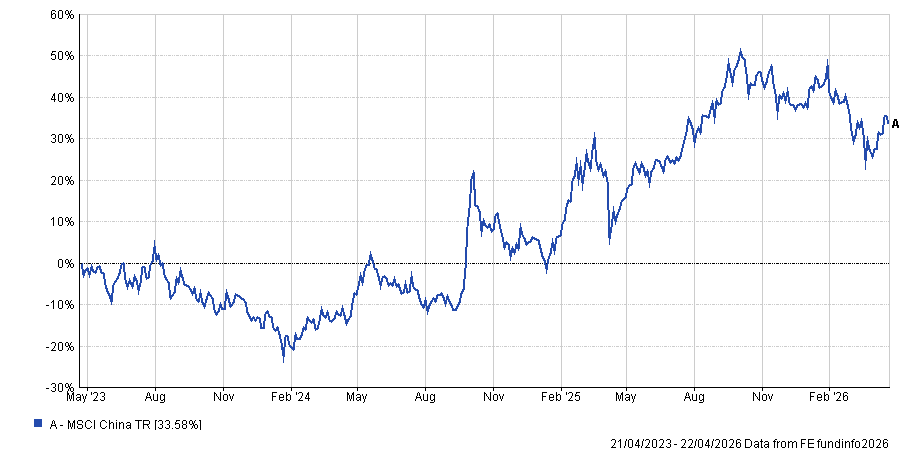

Performance of index over 3yrs

Source: FE Analytics

The bear case

“If you look at the last 30 years, China has had incredible economic growth, but investors have made no money at the index level,” he said. “The government does not allow excess returns. When companies become too powerful, they are curtailed.”

This, he argued, undermines the basic premise of equity investing: “Earnings growth has been weak, so while valuations look cheap, it’s a value trap. And then there are also the economic and geopolitical risks.”

For Jain, low valuations alone are not sufficient if the underlying earnings do not compound.

“China shows that GDP growth does not always translate into investment returns due to competition and government intervention. People can’t focus on low valuations and ignore long-term returns,” he said.

This perspective has led GQG to step back from the market. While the firm has invested in Chinese equities in the past, the manager said this was always contingent on strong earnings growth at the company level.

“We owned Tencent when earnings per share were growing 20 to 30%. Now growth has slowed. Many large-caps lack growth. Alibaba’s revenue has grown mid-single digits and earnings have declined due to margin pressure.”

“You have to look at a growth-adjusted basis,” Jain said, and from that perspective, other markets score much better: Indian banks pay 13x on a price/earnings-to-growth (PEG) basis and are growing 15% a year; US banks trade at 16 times earnings, growing 7% a year.

But to the comparison with India Jain adds another point: “The problem is, one is a communist country where you’re not allowed to make excess returns, and the other is not.”

The bull case

Qian Zhang, emerging market investment specialist at Baillie Gifford, takes a different view. While acknowledging the challenges, she argued that broad generalisations risk overlooking the diversity of outcomes within the market.

“One of the key things we learnt from more than 30 years of investing in Chinese companies is that generalisations about China are often unhelpful for long-term stock pickers,” she said. “The country certainly operates with a government system that is different from the West but there are a lot of nuances beneath the macro headlines.”

Zhang pointed to the concept of “common prosperity” as an example often misinterpreted by investors.

“It isn’t simply an anti-profit doctrine and its practical impact can be seen as more of a Chinese-style rebalancing, tilting away from property and leveraged construction and toward sustainable growth while still relying on an innovating private sector to deliver employment, technology leadership and consumer outcomes,” she said.

Private enterprise remains central to that model as more than 80% of the urban employment in China is offered by the private sector. “It is vitally important for policymakers,” she said.

At the same time, Zhang acknowledged that policy intervention can be a “a double-sided sword”, creating both opportunities and risks. On one hand, state support can intensify competition and create overcapacity, meaning not every company benefits and consumers may gain more than shareholders in some sectors.

On the other hand, the same forces can accelerate the development of leading businesses, she argued. “When top-down policy support meets strong bottom-up entrepreneurship, it can accelerate innovation, lower production costs and strengthen the global competitiveness of the best companies.”

The key is to be selective. Baillie Gifford believes the best opportunity is in the small number of businesses with the scale, efficiency and competitive edge to emerge as winners from a tougher, policy-shaped environment.

Zhang also challenged the idea that Chinese equities lack earnings growth altogether.

“The historical problem was that earnings per share lagged because of persistent share dilution, whereas that dynamic is beginning to change,” she said.

“Internet platforms are generating decent profits while still trading on moderate multiples; companies such as [EV manufacturer] BYD and [battery provider] CATL are using scale, product strength or cost leadership to take share in very large markets.”

The broader policy backdrop, in her view, reinforces these trends. “China’s policy support for industrial upgrading, digitalisation and green technology may compress but it also sharpens the edge of the winners and lowers the cost of building businesses through better infrastructure, logistics, automation and energy systems,” she said.

For investors, the key question is how to distinguish between genuine opportunities and value traps and Zhang had a formula for that: asking whether a company can continue to grow profits while being aligned with China’s broad economic development goal.

This requires a high level of selectivity and ongoing scrutiny: “The implied red line is not any state involvement, but the point at which governance, capital allocation, supply-chain integrity or strategic direction are no longer consistent with minority shareholder outcomes.”

This, at least for Baillie Gifford, leads to a concentrated approach to the market. Out of more than 6,000 listed Chinese companies, its strategies invest in fewer than 100.