The sterling strategic bond sector is marketed as flexible and unconstrained – a one-stop solution for investors who want to outsource their fixed income allocation to a manager with a wide mandate. But according to Mike Riddell, who runs the £241.9m Fidelity Strategic Bond fund, the reality is different.

“We’ve managed to almost perfectly replicate the average strategic bond fund over the past eight years by looking at a portfolio with 60% in an investment grade bond ETF [exchange-traded fund] and 40% in a high-yield bond ETF,” he said, as is shown in the chart below.

Investors often buy strategic bond funds because they want diversification away from equities, but this 60/40 mix of investment grade and high yield credit “does not provide that, as high yield correlates closely with equities, particularly in downturns”.

Rebased performance of peer group average returns and a blend consisting of 60% Global corporate Bond ETF and 40% Global high Yield ETF

Source: Fidelity International

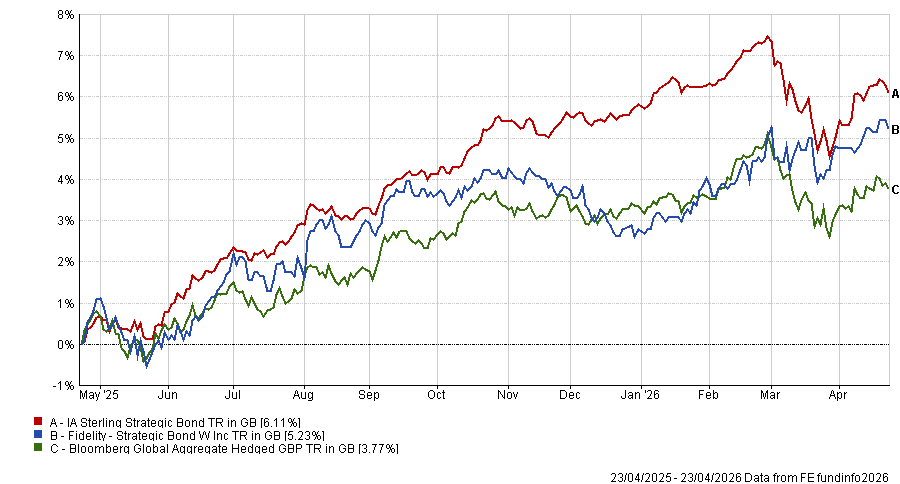

Riddell joined Fidelity 18 months ago after 12 years at M&G and nine at Allianz Global Investors, where he also ran a strategic bond strategy. He relaunched the Fidelity Strategic Bond fund in December 2024 with a different benchmark – the Bloomberg Global Aggregate hedged to sterling, an index that is entirely investment grade and predominantly sovereign – and a target of beating it by 2 percentage points per year.

In 2025, the fund returned 4.6% – 78th out of 89 funds in the IA Strategic Bond sector – as equities rallied and credit spreads tightened, conditions that structurally disadvantage a fund running less credit risk than its peers. This year so far, its fortunes have reversed, ranking 4th out of 91 funds with a gain of 2.6%, against a sector average of 0.4%.

Below, Riddell explains what drove that reversal, how the fund is positioned and why he thinks the dollar will remain weak for another five to 10 years.

Performance of fund against index and sector over 1yr

Source: FE Analytics

The sector is marketed as flexible and unconstrained. You’re saying most funds aren’t. How is yours different?

We use the global aggregate bond index hedged to sterling as our benchmark. That’s our neutral exposure. That index is entirely investment grade and most of it is sovereign, so we don’t have much credit risk in our portfolio to start with. We’re much less invested in credit and much less correlated to equities than the peer group.

We also really do use the flexibility the sector offers. We use top-down macro to get the big picture right on global growth and inflation and we have the full range of tools across rates, credit, inflation and currencies.

The two areas where we’re particularly different are inflation and currencies. We can take long views and go short. We actively use FX [foreign exchange] to drive returns and express global macro views. Most funds in the sector tweak slightly between investment grade and high yield.

Why should investors pick this fund?

If you own a typical strategic bond fund, you own a corporate bond fund. It will behave like equities in a downturn. Our benchmark is deliberately more defensive. We are trying to be a genuine diversifier, which is what most investors think they are buying when they buy this sector.

The alpha target is 2% per year above the benchmark. We’ve already exceeded that since we relaunched in December 2024. We also outperformed strongly in 2026 when conditions have been difficult for risk assets, which is when a defensive fixed income fund should add value.

What have been your best calls since the relaunch?

Last year, being bullish on emerging market currencies and emerging market local currency government bonds was the biggest driver of returns.

This year, the biggest driver has been our long inflation position.

In February, government bonds everywhere began to have a huge rally. This increasingly did not make sense to me because global economic data was coming in better than expected. From around mid-February, we began to see signs of concern in the oil market, oil prices beginning to move higher, yet no other market noticed.

It got to the point at the end of February where it was almost a free option to position the fund for a conflict to escalate, because markets were pricing in no risk of this happening. And so we de-risked: long inflation, short duration, out of emerging markets.

When the crisis hit, we made money on the increase in market-implied inflation, did well with bond yields rising and our credit shorts helped as spreads widened.

And the worst?

Inflation positions hurt in the last four months of 2025. We were long inflation on concerns about central bank credibility, but oil prices moved lower and that unwind hurt.

We also lost around 30 to 40 basis points on Colombia in Q4. We’ve since made that back. Being bearish on developed market credit detracted but that was the other side of being long emerging markets rather than a standalone call.

How is the fund positioned now?

We have the longest duration position since the middle of last year. UK, Norway, Australia and Canada are our biggest long positions, along with baskets of emerging markets including Brazil, Colombia and Peru. Government bonds are attractive as yields are still elevated.

In the UK, I've never seen such a big swing in Bank of England rate expectations. The market moved from pricing rate cuts to pricing rate hikes very quickly. If those hikes don't materialise, there is a decent capital gain available.

We are keeping some inflation protection, particularly in the US, where the market is pricing CPI at around 2.7% over the next two years. We think it could be above 3%.

On the dollar, we think we could be looking at five to 10 years of weakness, which supports the structural case for emerging markets. That is a long-term trade and we think it has further to run.

What do you do outside of fund management?

Sports and music. When I was 11, I was close to a world record for long jump. Now I organise a mixed touch rugby team at Fidelity and we play in a league. On music, I used to play in a band. I play piano, keyboard and guitar. I’d say a pub-standard musician.