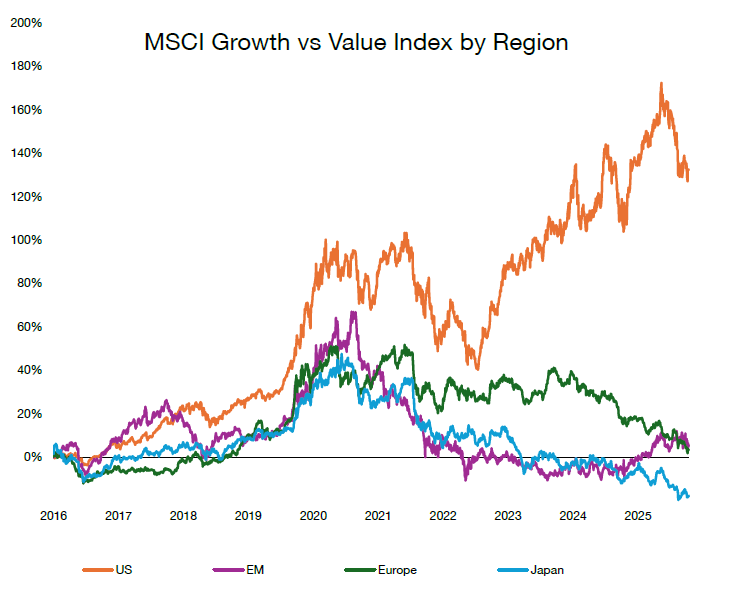

Growth has been the most profitable way to invest in many major markets for more than a decade, but there is one place where the recent fortunes have proven so dire that once popular companies have dropped to valuations that make them cheaper than rival stocks.

The chart below shows the returns from a range of MSCI indices, measuring the relative returns between the growth and value versions of different markets.

Matthew Brett, manager of the Baillie Gifford Japan Trust, said: “From 2016 into Covid, growth was generally the place to be across pretty much any market.

“Then after Covid, we had a couple of years where growth was definitely not the place to be, as various things reopened post‑Covid and more cyclical value‑type businesses did very well.”

From around 2022 markets then diverged. While growth has led the way in the US, reflecting the rise of the Magnificent Seven in this new AI era, it has been a different story elsewhere in the world.

While there has been little to choose between growth and value in Europe and the emerging markets, in Japan “value has been the thing to own” since 2020, Brett noted.

Source: Baillie Gifford

Growth investing has been challenged in recent years for three reasons, the Baillie Gifford Japan Trust manager said. Firstly, there was a rise in the cyclical industries and in particular exporters, such as industrials, auto manufacturers and banks, which all benefited after Covid as Japan finally started to see inflation for the first time in decades.

Additionally, a weaker yen has helped, as it has made the price of Japanese goods more appealing to overseas buyers.

“The exchange rate is roughly 160 yen to the dollar today. During the global financial crisis, it got to roughly 80 to the dollar. So a really big weakening of the yen has fuelled more export‑oriented businesses,” he said.

Lastly, a focus on governance improvements over the past 10 to 15 years has boosted large-caps in 'old economy' industries where there is a plethora of cash.

“Those have dominated the recent period in Japan — things like industrials, shipping companies, steel companies, car companies and so on,” said Brett.

This is all tied together by momentum, which he said plays a role as companies performing well tend to attract new money more easily.

However, he warned that “it’s quite likely that the best opportunities have gone far enough in that space now” and investors may not get the same level of returns moving forward as some of this has played out.

Firstly, he noted that the implied growth rates for the market are ambitious. While he is projecting sales growth of 7.9% and earnings of 12% per year for companies within his trust, sell-side analysts have consensus expectations of 2.7% sales growth and 10% earnings rises for the market.

“I personally think the 10% per year for the market as a whole will be quite challenging, given that it has already delivered annualised returns of around 16.3% over the past five years,” he said.

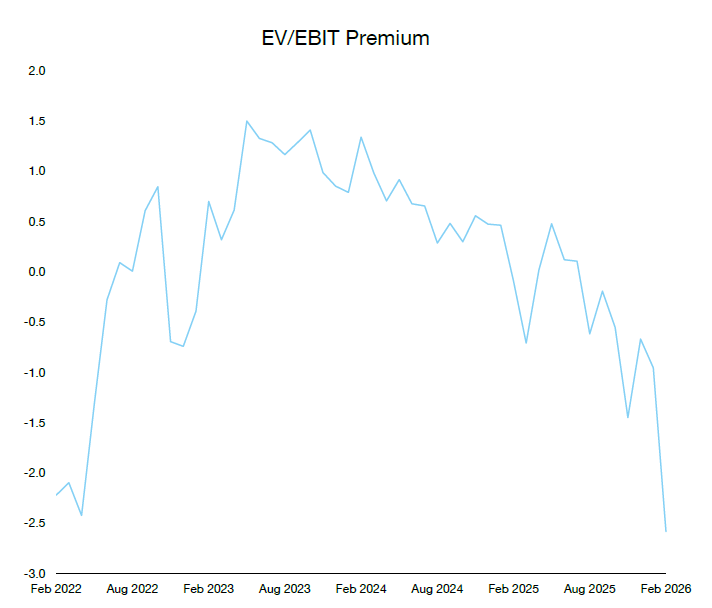

Next, Brett looked at the enterprise value (EV) to earnings before interest and tax (EBIT) ratio as a measure of relative cheapness, comparing his growth portfolio to the wider Topix index.

At the end of February, the market EV to EBIT was 17.2x, while the portfolio was at 14.6x, so roughly a two percentage-point discount.

Source: Baillie Gifford. Based on the Baillie Gifford Japan Trust vs Topix.

“The Japan Trust has gone to a discount to the market, both on a P/E [price-to-earnings] basis and on an EV to EBIT basis, at least as of February. This is a very rare situation,” he said.

While it is “normal” for his companies to trade at a premium to the market, trading on a discount is something that has only happened “a couple of times” in his career.

“I think that presents a fantastic opportunity in Japan for a growth‑oriented investor,” he said, adding that he is “surprised it [the value rally] has gone on as long as it already has” and suggesting that a potential catalyst for growth to return to the fore could be if valuations among cyclical companies become too stretched.

Another, he noted, could come down to the macroeconomics. “Over longer time periods, we’ve typically generated more relative performance when global economic conditions are tougher rather than when they’ve been very strong. I’ll leave it to others to decide what kind of macro environment we’re heading into,” said Brett.