The gap between cash holdings and equity exposure is near a record high as UK households have shunned markets in favour of the security of a bank account.

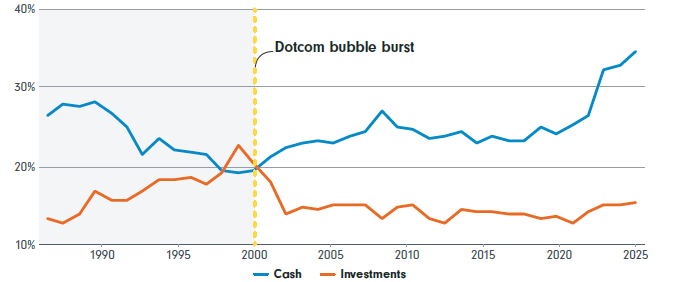

UK households’ propensity to invest actually peaked prior to the dot-com bubble of the late 1990s – a level they have failed to match in the 25 years since.

Around 23% of UK household financial assets were held directly in investments such as shares and funds outside pension wrappers in 1999, compared with just 17% at the end of 2025, according to analysis of government data by Fidelity International.

Over the same period, cash holdings have risen to 35% of financial assets, the highest proportion since records began in the 1980s.

The findings, published in Fidelity's report Rebuilding after the bubble, suggest the dot-com crash may have left a structural mark on UK investing behaviour that persists a quarter of a century later.

Marianna Hunt, personal finance specialist at Fidelity International, said: "Despite strong global equity returns in the decades since, households have not meaningfully rebuilt direct exposure to markets. Since the early 2000s, UK households have been net sellers of investments in most years, even through periods of recovery."

Between the start of 2001 and the end of 2025, UK households were net sellers of more than £566bn of investments. In 22 out of 25 years, households sold more than they bought.

Fidelity estimates that if UK households today allocated 23% of their financial assets to direct investments – matching the 1999 proportion – there would be approximately £414bn more invested in markets. This figure is based on total household financial assets of around £6.6trn and is equivalent to roughly 14% of UK GDP.

Hunt cautioned that the dot-com crash is unlikely to be the sole factor behind the shift from equities to cash. "Over this period, an ageing population, an increase in the costs of housing and changes to workplace pensions could all have played a part in shaping attitudes towards investing, risk and how assets are held," she said.

She also noted that the steady increase in equity ownership in the late 1990s was partly driven by the stock market bubble developing at the time, when speculation fuelled unsustainable company valuations and “shouldn't be treated as a 'golden era' for investing”. Still, the overall picture shows an investing culture that has never fully healed previous scars.

"Even after years of market recoveries, households have remained cautious, holding far more cash and taking on less direct exposure to long-term growth assets," Hunt said. "While that caution is understandable, it's important that households understand there is risk, too, in remaining in cash."

The UK's trajectory contrasts with other major economies. In the US, household investment levels are now significantly higher than in the late 1990s, Fidelity noted.

Percentage of total household financial assets

Source: Fidelity International

Three areas for reform

Fidelity highlighted three areas it believes require practical reform to address the investment gap.

First, more balanced risk warnings. The firm argued that risk disclosures should clearly communicate both the risks and long-term benefits of investing, suggesting that overly one-sided warnings risk deterring participation and reinforcing excessive cash savings behaviour.

The Investment Association's Risk Warning Review group, of which Fidelity is part, has proposed a framework for reform that maintains consumer protection standards while supporting confident participation.

Second, a national commitment to financial education. Fidelity called for financial teachings to be embedded across all life stages – from schools to workplaces to retirement planning – through a national strategy combining curriculum reform, employer engagement and clearer industry standards.

Third, a policy environment that actively encourages long-term participation. Fidelity said government and regulators should ensure tax, product design and communications consistently support long-term investment rather than unintentionally biasing households toward cash.

The firm pointed to global research showing that simplicity, compelling tax incentives and lack of restrictions on asset allocation are critical in building investing confidence.

The firm also called for policies to mitigate the impact of Budget speculation and to remove friction in moving from cash to investments.