The investment characteristics of America's largest technology companies have fundamentally changed, according to Felix Wintle, manager of the Tyndall North American fund, who worries about the impact of their spending on their investment case.

Wintle is making a call for 2026 that the so-called Magnificent Seven – Apple, Microsoft, Google, Amazon, Meta, Nvidia and Tesla – will no longer dominate market returns as they have in recent years.

"They are great companies," he said. "But they've gone from being cash flow machines with high margins to spending heavily and becoming cash flow negative."

Meta is spending all of its free cash flow this year on capital expenditure and the stock is underperforming as a result. Oracle, which is spending heavily to compete in data centres, is down about 30% over the year to the beginning of April 2026.

"Across the group, they're spending all this money and no one is seeing a return. The Mag seven as a theme isn't as strong as it was in previous years," he said. "It's not that we won't own them, but right now we think there are better opportunities.”

Tyndall North American is around 20% underweight the Magnificent Seven compared to the S&P 500 index. The positioning comes with risk, particularly after the fund underperformed in 2023 because of a similar bearishness, as the mega-cap tech names recovered strongly.

"At the end of 2022, after a big bear market in tech where the Mag Seven fell a lot, I felt they were kind of over," Wintle said. "But in 2023 they recovered at the expense of everything else in the market and that was a mistake on my part, to count them out too quickly. So it's not that I'll never own them. But right now I think there are better places to be."

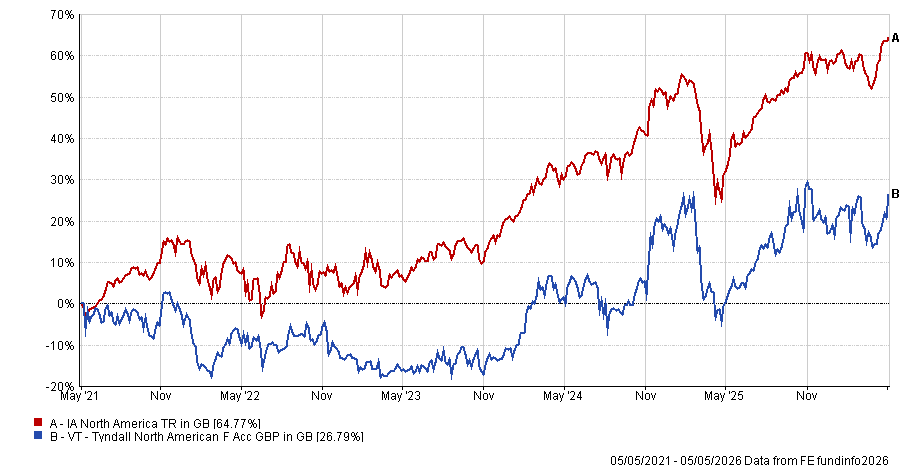

Performance of fund against index and sector over 5yrs

Source: FE Analytics

The shift away from the Magnificent Seven comes at a time when Wintle believes the US economy is in a strong position.

"When you look at what's going on in corporate America and in the US economy itself, it's actually a really bullish picture," he said. "We're going through a very strong, almost golden moment in the US economy of low inflation and high growth."

He expects nominal GDP growth to be north of 5%, a huge number compared with Europe and the UK, which are broadly flat. "Versus developed market peers, the US is a significantly better investment destination based on economic growth," Wintle said.

So while the biggest names in the American index are doing all the spending, the beneficiaries are smaller names that aren't heavily represented in passive indices, according to Wintle. "That's where we want to invest," he said.

His choice today is to back the beneficiaries of someone else's capex spending – one example being memory storage manufacturer SanDisk.

"There's a real bottleneck in memory and storage because of all the data being produced by data centres," Wintle said. "That data has to be stored and there isn't enough capacity."

DRAM and NAND are the two main types of memory and supply is constrained. Companies like SanDisk, SK Hynix and Samsung are among the only manufacturers and they have doubled prices multiple times.

Wintle also recently bought Intel, which is benefiting from strong demand for CPUs as well as GPUs.

"For agentic AI to take off, you need both," he said. "This is a new cycle. Intel has been a dormant company, but suddenly there's demand for CPUs again."

The company reported a much larger gross margin than expected because it was able to sell inventory at full price. Since the position was initiated on 22 April, the stock has grown to a top position in the fund.

"It's not a big part of the S&P anymore, so it's a good opportunity to be different and add alpha," Wintle said.

Price of stock over the past 6 months

Source: Google Finance

Outside tech, the US consumer offers "selective opportunities". The fund recently bought back Starbucks after the company went through a difficult period with poor service and a confusing menu.

"They've got a new management team now," he said. "It takes time to turn things around, but they reported strong numbers, 7% comp growth, which is really strong. We look for those inflection points as companies start to recover."

The fund also owns Warby Parker, which is developing AI glasses with Google. "It could be one of the first big consumer AI products that people really take to," Wintle said. "For a company like Warby Parker, it could be transformational."

Tyndall North American also has around 10% in energy, well above the index weighting, reflecting the manager's view that a new cycle is developing.

"There's damage to infrastructure and supply chains, and a need for new sources of energy," he said. "That creates opportunities in repair and new build. Most generalist funds wouldn't have that, but that's how we differentiate, by investing where we see the best opportunities even if it's out of line with the benchmark."

In the last 12 months, the positioning has benefited the fund, which is up 25.2% in the timeframe, against the 22.4% average return of the IA North America sector.

Wintle isn’t alone in his decision to broaden out within the US. Earlier today, Trustnet revealed which non-Magnificent Seven are the most owned in the IA North America sector.

That said, there are some of the Magnificent Seven that Wintle likes, as he said there is "a real dispersion of returns between these companies, so it's right to assess them individually rather than as one group".

The fund owns Nvidia and Google parent Alphabet among its top 10 positions – and these are also in the top three of the most-owned Magnificent Seven companies across the IA North America sector, as Trustnet revealed this week.

"The key driver for Alphabet is cloud growth. Google Cloud is growing 63% and taking share. You also have YouTube, the G Suite and other businesses, plus AI through Gemini. It's a diversified business with strong growth drivers,” he concluded.