Record highs in US stocks have divided market analysts, with some seeing rational pricing of AI growth and geopolitical risk while others warn that stretched valuations, narrow market breadth and a technically driven short squeeze may be doing more of the heavy lifting than investors realise.

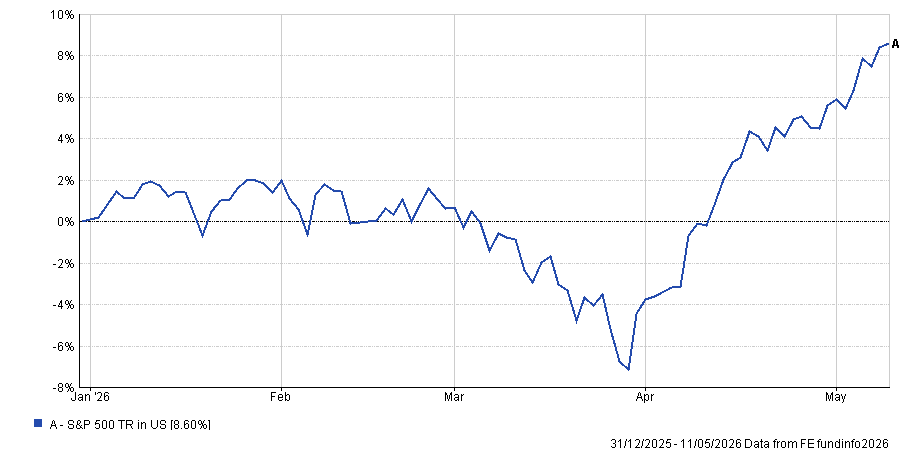

The S&P 500 has brushed aside March’s brief sell-off, which followed the outbreak of war between the US and Iran, and pushed to new all-time highs. Only Japan and Brazil have delivered better returns over the past year.

Performance of S&P 500 over 2026

Source: FE Analytics. Total return in US dollars between 1 Jan and 11 May 2026

The BlackRock Investment Institute sees no inconsistency in markets rising alongside elevated oil and yields, arguing that artificial intelligence is doing the offsetting work.

However, AJ Bell investment director Russ Mould took a more cautious view, calling on investors to stress-test the reasons for their optimism before concluding the good news is not yet priced in.

BlackRock’s bull case rests heavily on the AI earnings story: expected S&P 500 earnings growth for the first quarter has climbed to around 28%, roughly double early-April estimates. Meanwhile in the MSCI emerging market index, tech earnings growth expectations have jumped to around 160%.

The Magnificent Seven are tracking a 57% jump in quarterly earnings, three times higher than Bloomberg consensus estimates from just a month earlier, BlackRock noted. Nvidia is yet to report.

Capital spending across the Magnificent Seven is now estimated to reach as much as $725bn this year, up around 10% from pre-earnings forecasts.

BlackRock added that an emerging AI-driven cybersecurity arms race is sustaining demand for compute, cloud infrastructure and advanced models, reinforcing the growth trajectory.

Mould’s data pointed in the same direction for earnings: FactSet consensus forecasts put S&P 500 earnings growth at 19% for 2026 and 16% for 2027, with the technology sector leading at 38% and 25% respectively.

Geopolitical de-escalation has also played a role in the US market’s rally. Washington-Iran talks have begun and a ceasefire has been declared. If the risk of further escalation has passed, Mould argued, investors can refocus on the prospect of interest rate cuts under incoming Federal Reserve chair-elect Kevin Warsh in 2027 and on Republican efforts to boost the US economy ahead of the 2028 presidential election cycle.

A short squeeze has added near-term fuel and acts as a warning sign. Goldman Sachs research showed that algorithm-driven and hedge funds were short in mid-March, so the rally forced them to cover positions and created what Mould described as “a multi-billion-dollar short squeeze”.

“A surge in the Refinitiv Most Shorted stocks index backs up the final argument and hints that the US equity rally may be technical, rather than fundamental, in origin,” Mould said.

“That in turn suggests the foundations of the rally may not be as strong as they seem, especially as much rests upon AI delivering lofty productivity gains and returns on investment, and market breadth is narrow.”

Mould acknowledged the structural case for a US valuation premium: it is the world’s deepest capital market, has reserve currency status, a light regulatory touch, a corporate environment that prioritises quarterly earnings and the 401k savings culture.

“However, none of this is ‘news’, as such, and dangers do still lurk,” he added. “The key now is to stress-test those reasons, check out their durability and reassess the ultimate arbiter of investment return, which is valuation. Is the good news already priced in or not?”

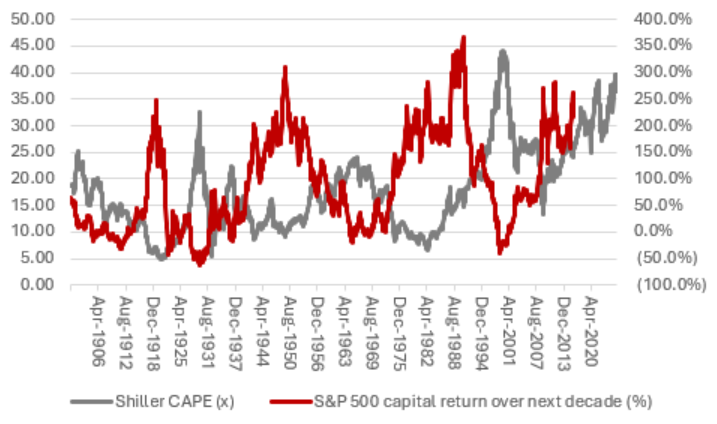

On that measure, the picture is less comfortable. FactSet earnings estimates put the S&P 500 on a forward price/earnings ratio of 21 times, above its 20-year average of 19 times. The cyclically adjusted price/earnings (CAPE) ratio devised by professor Robert Shiller, which takes a 10-year inflation-adjusted view, is at historically elevated levels.

Shiller CAPE ratio and S&P 500 returns over following decade

Source: AJ Bell, Robert Shiller data

On valuations, BlackRock argued that equity markets are balancing growth against rates and that strong enough earnings growth can offset higher yields, as the post-ChatGPT surge has demonstrated.

The risk, in the asset management giant’s view, is that if disruptions persist, the combined pressure of higher inflation and rising capital demand could push yields high enough to weigh on valuations and tighten financial conditions, ultimately challenging both risk assets and the pace of the AI buildout itself.

“The AI buildout has so far outweighed the typical effect of a macro shock: a drag on growth and earnings that hurts equities. That leaves interest rates as the key mechanism through which the shock could challenge risk assets,” BlackRock’s strategists said.

Both BlackRock and Mould agree that AI must deliver. BlackRock’s pro-risk positioning, which includes overweighting US and emerging market equities while remaining underweight long-term US Treasuries, is explicitly conditional on the eventual re-opening of the Strait of Hormuz and the AI buildout continuing to outweigh macro headwinds. Mould flagged AI productivity returns as the critical variable beneath current multiples.

The Magnificent Seven now account for $23.6trn in aggregate market capitalisation, equal to 37% of the S&P 500’s total. The group provided 53% of the total increase in the index’s market cap over the past year and 40% of the increase in 2026 to date.

“Such narrow markets either tip over or see investors seek to rebalance in the end, but no one knows when or where that tipping point rests,” Mould said.

“The technology, media and telecoms bubble did not peak until March 2000, after all, and it only did so when failure to meet lofty earnings growth expectations bumped into equally lofty valuations.”