The board of Finsbury Growth & Income trust is set to more than triple down on FE fundinfo Alpha Manager Nick Train by upping the trust’s gearing from £29.2m to its full £100m allocation.

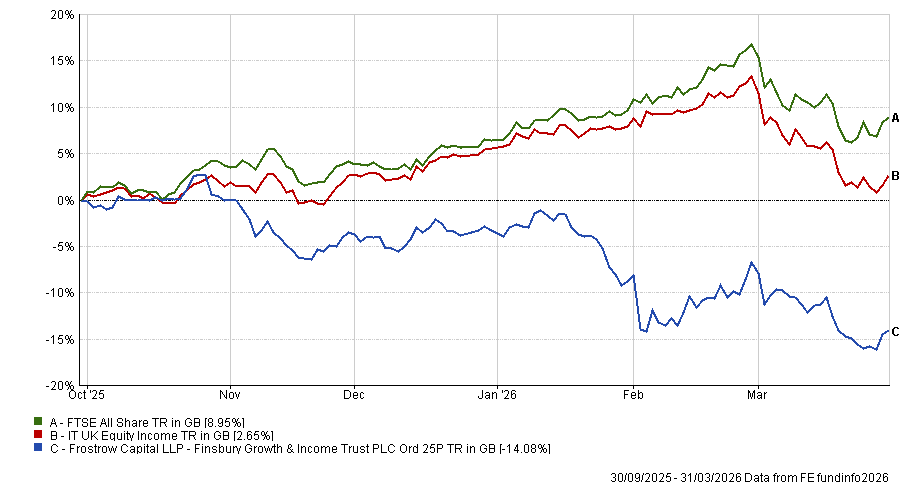

It comes after the trust suffered a share price total return of -14.1% in the six months to 31 March, which was slightly better than the net asset value (NAV) performance of -14.4% as share buybacks lifted the discount slightly.

Pars Purewal, chair of the trust, said: “While recent performance has been disappointing, we are seeing early signs of stabilisation and remain firmly committed to the portfolio manager's disciplined, long-term approach focused on high-quality businesses with resilient franchises and hard-to-replicate data assets, where we believe AI will prove an enhancer of value rather than a threat.”

Performance of trust vs sector and benchmark over 6 months

Source: FE Analytics. Data to 31 March 2026.

Upping the trust’s gearing will give Train more money to invest at a time when many of his holdings have fallen, particularly London-listed data, software and platform companies, where he said there is a “once-in-a-decade opportunity” to buy at “fundamentally the wrong price”.

“Writing this report reinforces our conviction that your portfolio is comprised of a collection of outstanding, in most cases world-class, UK-listed companies that have, for a variety of reasons, fallen out of favour with investors,” he said.

“This really should be an opportunity to utilise the special powers of an investment trust to create additional value for its shareholders.”

It was not the only change made in the most recent results, however, with the trust also adopting an enhanced dividend policy from its next financial year.

From October, the annual dividend will increase by at least 50% from approximately 20p to 30p per share, raising the current yield from around 2.6% to 3.9%. Future dividends will be set on a pence per share basis rather than by reference to NAV or share price.

The board also highlighted the previously agreed reduction in management fees, which came into effect at the start of 2026 and has saved investors £129,000 over the first quarter of the year.

Purewal said: “Against a backdrop of compelling UK valuations, our confidence in the company's prospects is growing and the board remains committed to doing whatever it takes to improve shareholder outcomes through disciplined investing, active balance sheet management, an enhanced dividend policy and careful discount management.”

Matthew Read, senior analyst at QuotedData, said the poor performance of recent years “demanded a response” from the board.

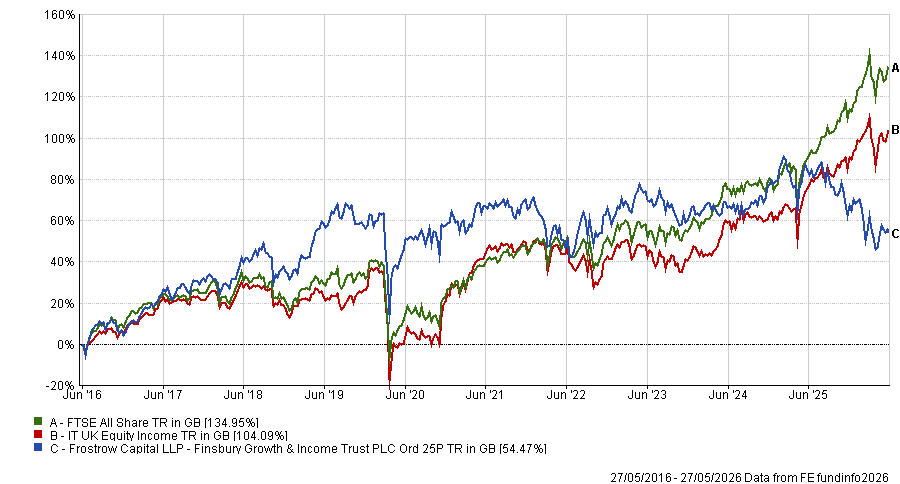

To the end of March, the trust has made just 49.1% over the past decade and has lost investors 5.4% over five years – the second-worst performance in the IT UK Equity Income sector.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics. Data to 31 March 2026.

However, much of this relative poor performance has come in the past year, in which the trust has been the worst performer, cancelling out strong years such as its FY results to 30 March 2022 and 2019, when it was the best performer in the peer group.

“The rebased dividend lifts the trust’s yield to around 4%, bringing the trust into line with its UK equity income peers. One long-running niggle we had was that the yield was not really high enough for the UK equity income sector; this fixes that,” said Read.

He described the increase to gearing as “the clearest statement of intent” that the board is “doubling down to exploit what they see as a valuation opportunity in the aftermath of the ‘SaaSpocalypse’”.

Investors should be aware, however, that the trust is becoming a more binary play on software than it has previously. Read noted that if Train is right and data, software and platform businesses become more valuable in the AI era rather than being eviscerated by the new technology, “current valuations could prove anomalously cheap”.

“If he is wrong, gearing into the same portfolio could compound the pain,” he said.