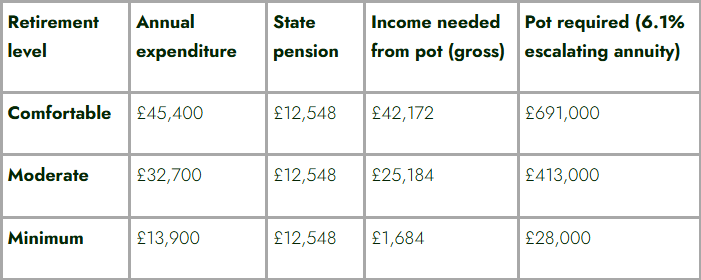

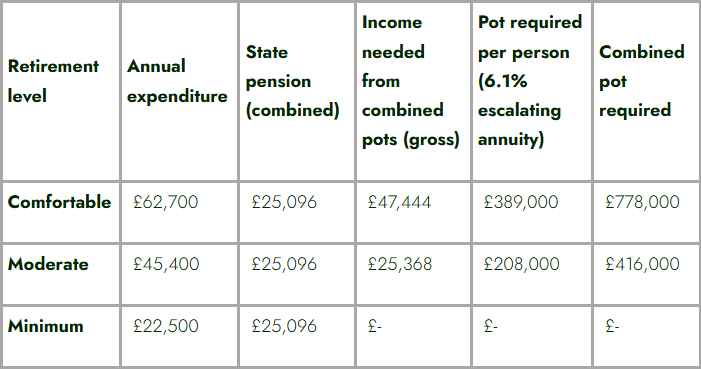

A single person now needs a pension pot of £691,000 to achieve a comfortable lifestyle in retirement, while a couple requires £389,000 each, according to wealth manager and financial adviser Quilter.

This has been calculated against the latest Retirement Living Standards (RLS) report published by Pensions UK, which outlines the additional private pension income needed for minimum, moderate and comfortable lifestyles in retirement, based on real-world spending patterns. Its calculations assume receipt of the full state pension and no rent or mortgage costs.

According to the RLS thresholds, a minimum lifestyle now costs £13,900 a year for a single person and £22,500 for a couple. A moderate lifestyle requires £32,700 or £45,400, while a comfortable lifestyle has risen to £45,400 and £62,700 a year respectively.

With the full state pension now sitting at around £12,500 a year, this comes close to supporting costs at the minimum threshold for single people or couples of its own.

To determine the size of the pension pot required to generate an income level with each of these thresholds, Quilter based its calculations on a 6.1% escalating annuity rate for a 66-year-old – also assuming no housing costs in retirement.

For a single person, Quilter’s calculations yielded the following.

Source: Quilter

Quilter’s estimations for joint pot sizes are also shown in the table below.

Source: Quilter

Pensions UK expects 82% of the working population to reach the minimum standard of living in retirement, compared to 23% reaching a moderate standard and just 9% achieving a comfortable lifestyle.

Zoe Alexander, executive director of policy and advocacy at Pensions UK, said: “The latest update to the RLS underlines a clear reality for many people: today’s saving levels will not be enough for the retirement they expect.”

She warned that without action “too many risk facing a cliff-edge drop in income when they stop work”.

These thresholds do not match up with what pension savers expect, with the comfortable threshold for retirement practically double what people believe they need. According to interactive investor’s 2025 ‘Great British Retirement Survey’, pension savers said they believe they need to save an average of £350,000 for a comfortable retirement.

It is also important to note that the Quilter figures assume people are mortgage-free at the point of retirement – a reality that will become less common for future generations who are taking out larger mortgages with longer terms.

Jon Greer, head of retirement policy at Quilter, said: “Factoring in housing costs could push the required income higher still, making early planning and regular reviews even more important.”

Intensifying financial challenges also need to be accounted for when considering how the RLS applies to younger generations, in particular, with Gary Smith, retirement specialist at Evelyn Partners, warning that younger and middle-aged savers will need to further adjust their pension pot projections for inflation.

“If someone currently needs a post-tax income of £45,400 for a ‘comfortable’ lifestyle, they will need a lot more in 20 years’ time – if inflation averages 2.5% over the next two decades, that is roughly £74,800 by 2046,” Smith said.

There are also questions around the long-term sustainability of the state pension in its current form, he added.

“What is clear is that workers must think seriously about how much they are saving right now,” Smith said.

Recent research by AJ Bell shows the challenge for pension savers aiming for Quilter’s moderate lifestyle pension pot of £413,000 for a single person and £416,000 for a couple.

It said that a 30-year-old earning £37,000 today could build a pension pot of over £437,000 by age 67 by contributing 8% of their salary – assuming their employer also adds 3%.

However, this also assumes the individual already has £19,000 in pension savings, achieves a 5% annual investment growth before charges of 0.6% and receives a 3% pay rise each year.

For someone aged 40 with an existing pot of £39,500, they would need to contribute 11% of a £48,000 salary to get the same pot value.

For those aged 50, the task is even harder. AJ Bell assumed the saver would have an £80,000 existing pension pot, noting they would still need to contribute 18% of a £58,000 salary to reach Pension UK’s moderate living standard by state pension age.

Charlene Young, senior pensions and savings expert at AJ Bell, said: “These personal contribution figures rise to a whopping 16% (£493 per month), 22% (£880 per month) and 35% (£1,692 per month) of the respective salaries for our three age groups to get over £700,000 and into the pot range required for a comfortable living standard.

“Clearly the contribution from a worker could be lower if an employer paid in more than just 3%, but this also highlights that stark reality for self-employed people, who will not benefit from an employer top up.”

The AJ Bell research underscores how the current 8% auto-enrolment minimum is unlikely to be enough for future retirees – an issue that the re-established Pensions Commission is considering, with the body’s report expected next year.

Policy uncertainty is not helping matters, with pensions being dragged into inheritance tax from April 2027 and changes to salary sacrifice adding further complexity.

Craig Rickman, personal finance expert at interactive investor, said: “Moving the goalposts and chipping away at valuable tax incentives may disincentivise savers at a time when many need all the help, encouragement and support they can get.”