Today’s investing landscape reflect a macroeconomic regime very different from the one investors grew accustomed to following the global financial crisis. Shifts set in motion by pandemic-era imbalances, geopolitics, supply chain realignment, and a major pivot in monetary policy have proven enduring rather than cyclical.

Recent years have brought clarity and reaffirmed a central reality; the ‘old normal’ of near zero interest rates, muted inflation volatility and persistently low yields is not returning. Instead, we operate in a world of higher-trend inflation, frequent macro swings, and a more balanced distribution of returns across asset classes.

The composition of the regime shift has changed, though the direction remains the same: growth rests on a firmer foundation, supported by improving productivity and sustained investment in infrastructure and energy systems. Inflation is lower than the post-Covid peaks but is exhibiting stickiness, driven by structural forces including labour scarcity, commodity underinvestment, and the shift toward deglobalisation.

Equally important are the forces behind these long-term assumptions: normalising interest rates in recent years, elevated geopolitical fragmentation, physical resource constraints and the fading of the disinflationary tailwinds of the 1990–2019 era all remain firmly in place. Real yields remain meaningfully positive, inflation risks remain volatile and asymmetric to the upside, and we expect rotation of market leadership in coming years.

Investors have demonstrated a tendency to chase past winners, falling for the FOMO trap. However, the reality of market cycles suggests caution. Indeed, market leadership changes during different regimes.

In the early 2000s, real assets and bonds were clear winners, however in the last 15 years, equities and private assets dominated market leadership. As a result of the robust performance of US equities, valuations are now at near historical extremes. Yet the underlying reality is more nuanced: while technology-led growth is real, the cost of capital has structurally risen, input prices remain firm, and margins may struggle to remain at peak.

This is why rotation away from narrow US equity leadership and toward more attractively valued, more diversifying assets is stronger today than at any time since the early 2000s.

Real assets in particular stand out. Their combination of appealing valuations, strong inflation linkage and healthy fundamentals in supply-constrained segments positions them for a larger role in long-term portfolios. Infrastructure and natural resource equities benefit from multi-year investment cycles and supply discipline; commodities have experienced years of underinvestment; and listed real estate, having reset meaningfully, offers more balanced return prospects with improved income yields.

However, risks do remain, AI-driven productivity could disappoint or lead to structurally higher unemployment, while inflation could reaccelerate on renewed supply shocks. Geopolitical events may further disrupt global trade flows. Valuations across equities or private markets may adjust faster than expected. The bond market could also reprice the long-term neutral rate higher, or credit spreads could widen abruptly after a prolonged period of tightness.

Despite these, the macro backdrop and market setup provide the strongest foundation for rotation in more than a decade. With forward-looking returns shaped increasingly by starting valuations, cash flows and structural sensitivities, we believe the next decade will diverge meaningfully from the last and the greatest risk for investors is missing the broadening opportunity set.

Full 10-year capital market assumptions: Expected average annual returns vs. prior-decade annual returnsi

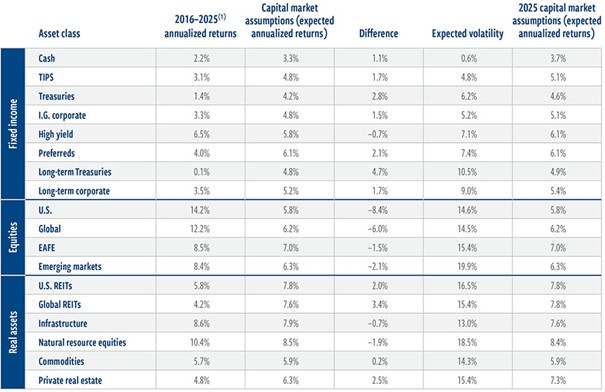

Macroeconomics: We expect the global economy to deliver moderate but stable growth over the next decade, with the US averaging 2.1% real GDP growth and global growth trending at 3.6% annually. We expect 1.8% trend productivity growth, partly linked to AI diffusion and ongoing investment in digital and physical infrastructure – offset by worsening demographics and episodic supply frictions. Consumer inflation is expected to average 3.0% annually in the US, well above the 1.6% experienced in the last cycle and significantly higher than the Federal Reserve’s long-term target. This elevated inflation reflects structural tightness in labour and materials, a more fragmented global trading system and geopolitical friction.

Fixed income: Interest rates are likely to remain higher than in the prior decade, with long term yields reflecting positive real rates and firmer inflation expectations. While absolute yields drifted lower during 2025, the long-term equilibrium for interest rates has reset meaningfully higher, offering investors a more attractive long-term fixed income return profile relative to the last decade.

We expect US government bonds to deliver solid, if unspectacular, nominal returns of 4.2% annually. Credit sectors will benefit from healthy economic and corporate fundamentals. However, today’s tight spreads and expected greater cyclical volatility suggest returns will be income driven, with little potential capital appreciation.

Equities: US equity returns, at 5.8% annually for the next 10 years, remain constrained by elevated valuations, slower-trend growth, higher input costs and a structurally higher cost of capital. We see better opportunities in developed non‑US equities, with returns holding steady from the prior forecast at 7.0%, as valuations are more compelling and earnings growth has room to normalize.

Emerging markets (EMs) remain a selective opportunity, with fundamentals varying widely across regions and sectors. EM equity returns are expected to be 6.3%, below their long-term historical average given the healthy gains of the last decade.

Real assets: 2025 was a reminder that real assets can perform well when other markets show strong returns. Most real assets categories were up more than 10%, and they stand out as one of the most compelling long-term opportunities today. We expect natural resource equities to lead with annual returns of 8.5%. Infrastructure is projected to return 7.9%, real estate 7.8 and commodities 5.9%, all supported by structural scarcity, inflation sensitivity and sustained investment needs. Valuations are attractive, fundamentals remain strong, and correlations with traditional stocks and bonds continue to offer diversification benefits.

Jeffrey Palma is head of multi-asset solutions at Cohen & Steers. The views expressed above should not be taken as investment advice.

i Past performance is no guarantee of future results. Forecasts are inherently limited. There is no guarantee that any market forecast will be realized. (1) 2016–2025 performance (01/01/2016–12/31/2025) represented by the following: Fixed income: Cash: Bloomberg U.S. Long Government/Credit Index. TIPS: U.S. Treasury Inflation Notes Index. Treasuries: Bloomberg U.S. Treasury 7-10 Year Index. Investment-grade corporate bonds: Bloomberg U.S. Corporate Investment Grade Index. High-yield bonds: ICE BofA High Yield Master II Index. Preferred securities: ICE BofA Fixed Rate Preferred Securities Index. Long-term Treasuries: Bloomberg U.S. Treasury Long Bond Index. Long-term corporates: Bloomberg Long U.S. Corporate Bond Index. U.S. equities: S&P 500 Total Return Index. Global equities: MSCI ACWI Total Return Index. EAFE: MSCI EAFE Total Return Index. Emerging markets: MSCI Emerging Markets Total Return Index. Real assets: U.S. REITs: FTSE Nareit All Equity REITs Index. Global REITs: FTSE EPRA Nareit Developed Real Estate Index. Global listed infrastructure: UBS Global 50/50 Infrastructure & Utilities Index (net) through March 31, 2015, and the FTSE Global Core Infrastructure 50/50 Net Tax Index for periods thereafter. Natural resource equities: S&P Global Natural Resource Equities Index. Commodities: Bloomberg Commodity Total Return Index. Private real estate: NCREIF ODCE Index. Volatility is represented by standard deviation, which is a statistical measure of the historical volatility of returns; the higher the number, the greater the risk.