It is “better the devil you know” when it comes to the UK government, according to Marlborough's Eustace Santa Barbara, who said it would be better for his investors if there was a political status quo rather than a leadership challenge.

This week is an important one for the Labour party. On Thursday 18 June, the Makerfield by-election could decide the future direction of the government.

Former Manchester mayor Andy Burnham is the Labour option on the ballot after ex-MP Josh Simons resigned so Burnham could run and, in turn, potentially take on Keir Starmer for the Labour leadership.

If Burnham wins, there is likely to be more uncertainty, something that markets notoriously dislike. This would impact Santa Barbara’s funds. He runs the IFSL Marlborough Special Situations portfolio, as well as two specialist small-cap funds.

This area of the market is more domestic-orientated and therefore can get buffeted around more by political instability.

“Starmer is doing a job. Rachel Reeves is doing a job. We, being the financial market, are sort of aware of what we're getting [with the current government],” he said. “For our unit holders, my suspicion is that the status quo would be a better outcome than Starmer losing.”

A Burnham challenge would add political instability. For starters, there are currently question marks over who would be his proposed chancellor.

“One of the front-runners, in terms of the betting, would be Yvette Cooper or Ed Milliband, who I would say holds some less market-friendly political and economic views,” the manager said.

That is not to say Santa Barbara is in lockstep with the current government either. He pointed out that there has been “some tinkering” and “rule breaking”, such as promising there would only be one painful, tax-hiking Budget.

“‘One and done’ suddenly became another tax-raising Budget,” the manager said, including recently foreshadowing that the Treasury may need raise more taxes to pay for defence spending and welfare increases.

“I'm [also] not exactly delighted by the lack of business experience on the front bench currently. I think that's a very obvious deficiency there. The lens from which they're looking at things is, shall we say, rather narrow? It does mean they're not great at thinking about consequences,” Santa Barbara noted.

Political instability is not new for UK investors, with the manager noting that it “hasn’t been a great decade” for political stability, with 2022 particularly “horrific”, with three prime ministers (Boris Johnson, Liz Truss and Rishi Sunak) and four chancellors (Sunak, Nadhim Zahawi, Kwasi Kwarteng and Jeremy Hunt).

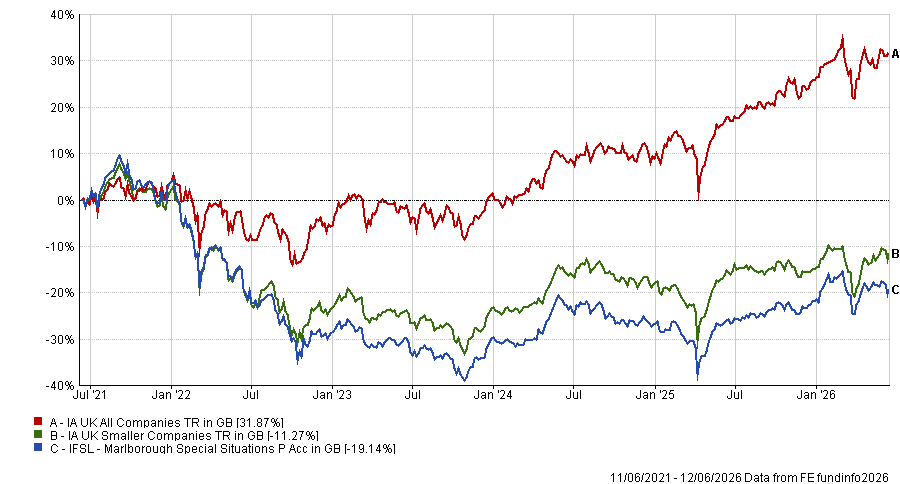

It is by no means the only thing that has held UK smaller companies back in recent years. Indeed, IFSL Marlborough Special Situations has been one of the worst performers in the IA UK All Companies sector over the past five years, down 19.1%, as small-caps have struggled.

Performance of fund vs sectors over 5yrs

Source: FE Analytics

Yet the manager remains optimistic, noting that it is “darkest before dawn”. Although “the cheap can always get cheaper” when it comes to the UK market, there are some assumptions that he believes simply do not hold true.

The first is the prevailing view among markets that the UK has low or no GDP growth over the next three to five years, which leaves a lot of potential for the economy to surprise to the upside.

Another is capital flows into the lower portion of the market. UK funds have suffered outflows for years and much of the underperformance of the mid- and small-cap segment of the market has been due to investor selling, rather than inherently poor performance by the underlying companies, he noted.

There were signs this was reversing earlier in the year, when money started to enter this part of the market in January and February, before abruptly U-turning following the outbreak of the Iran war.

“Flows have probably had an exacerbating negative impact on our stocks. But I'm just not seeing the outflows we've seen in recent years, which is a genuinely positive thing. I don't know many managers in my space who are looking to sell,” said Santa Barbara.

While “we're still in the earlier contrarian phase in terms of people deploying capital into this space”, once one buyer emerges and small- and mid-cap companies get attention “they can move very quickly,” he said.