Troy's Personal Assets Trust has lagged the market by a significant margin over the past year, but co-managers Sebastian Lyon and Charlotte Yonge believe the portfolio is better positioned than ever to weather the storms they see ahead.

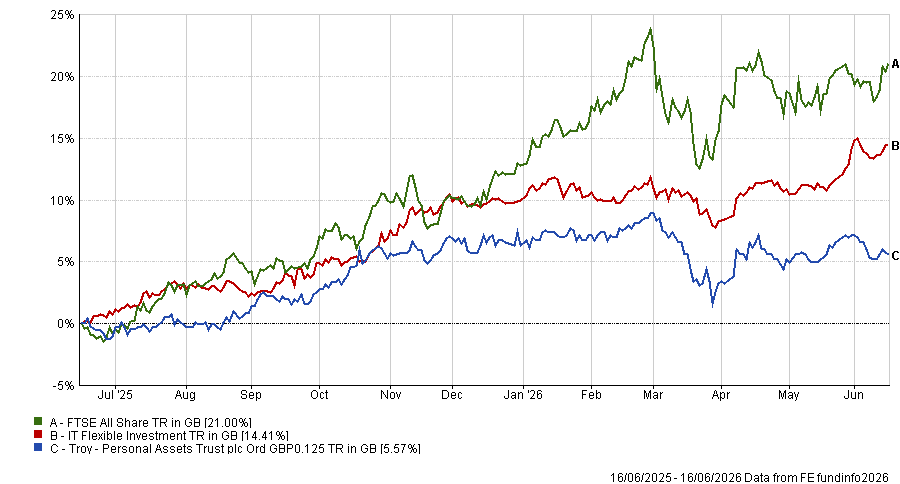

The trust returned 6.3% in NAV terms for the year to 30 April 2026, against 25.2% from the FTSE All Share, a gap the managers describe as 'uninspiring' but largely expected given the trust's capital preservation mandate.

Personal Assets is designed to protect and then grow shareholders' capital. With 36% of the portfolio in equities at the year end and the rest spread across index-linked bonds, gold, cash and – unusually – Japanese yen, the trust is not built to chase a rising market.

The yen position is the most prominent addition to the portfolio, with Lyon and Yonge initiating a roughly 10% holding through short-dated Japanese government bonds in 2025 – the first time the trust has held the currency – on the expectation of sustained US dollar weakness.

“The Japanese currency is the cheapest it has been for four decades and the dollar has risen by 55% against the yen since 2020, moving well away from purchasing power parity,” they said. The holding has so far made a modest loss but Lyon and Yonge are not concerned.

The yen has historically strengthened in crises, as investors unwind yen-funded borrowings and repatriate capital. According to BCA Research, yen-denominated claims in overseas financial centres amount to around $650bn. When risk assets sell off, that capital tends to come home – and the yen strengthens.

“We believe the holding will provide us with good diversification and an offset, should stock markets become more risk-averse,” Lyon and Yonge said.

A weak yen is also deepening Japan's cost-of-living crisis and the managers see growing political pressure to address it. That adds a second potential route to yen strength, independent of global risk sentiment.

The case for holding the currency is also based on the view that markets are underpricing tail risk. They pointed to the Iran conflict as the fourth material supply shock of the decade, after the pandemic, the invasion of Ukraine and last year's tariffs. Central banks – already struggling to reach inflation targets – are now facing stagflation again and stretched government balance sheets leave little room for a fiscal response.

“Markets appear remarkably complacent about the threats posed from the conflict in the Gulf,” Lyon and Yonge said. “If the Strait of Hormuz is not reopened soon, the tail risk of a stagflationary outcome may become an inevitability.”

Speaking to Trustnet last month, Yonge said that if we get to August without oil supply resuming, there's “a very real chance of recession”.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Against that backdrop, gold – held at 9% of the portfolio at year end – was up roughly 41% over the period and provided the bulk of returns outside equities for Personal Assets.

The equity sleeve, at around 36% of the portfolio, rose approximately 6% in aggregate. Alphabet, the trust's largest holding, rose 140% over the 12 months. Hubbell and Canadian National, both added during the year, rose 42% and 17% respectively. These gains were partly offset by sharp falls in Diageo and Experian, each down 27%.

The managers sold three positions during the period – American Express, Moody's and LVMH – and added Alcon, the eye care device company, alongside Hubbell and London Stock Exchange Group.

LSEG was flagged as one of the year's more interesting calls: the stock rallied from its February lows as the market came to appreciate the value of its proprietary datasets, which Lyon and Yonge argue AI will struggle to replicate.

AI is a thread running through the report. Lyon and Yonge described the market as moving fast to price in “unknowable change,” drawing a parallel with the internet boom of the late 1990s. They noted that following SpaceX, OpenAI and Anthropic are also expected to seek IPOs in the coming months, at valuations of $800bn and $1.3tn respectively – which they expect to sustain the pace of new model releases as those companies chase credible revenue streams.

Gold was reduced from 14% to 10% in January, when the price exceeded $5,100, on the grounds that purchasing behaviour had become “exuberant.” Lyon and Yonge remain positive on the position over the long term but trimmed on valuation grounds.

The board also agreed a revised fee structure with Troy, effective 1 May 2026, reducing the management fee on assets above £1.5bn from 0.45% to 0.35%.