Terry Smith lifted portfolio turnover of Fundsmith Equity to more than 50% in the first half of 2026, a high for the fund, as he adapted his investment approach to a market driven by passive flows rather than company fundamentals.

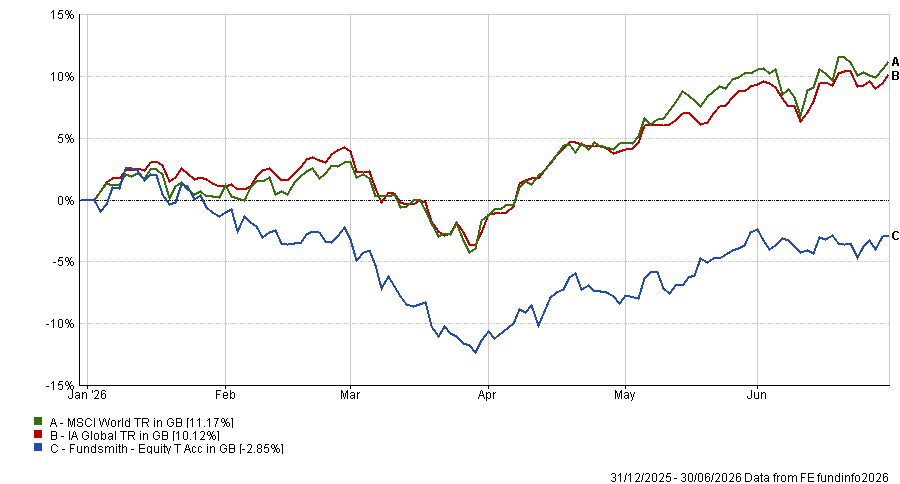

Fundsmith Equity lost 2.9% between January and June 2026, against a gain of 11.2% for the MSCI World index in sterling terms. Smith linked this backdrop to a market in which momentum, rather than profitability or returns on capital, increasingly sets share prices.

He cited figures from Cboe Global Markets showing active fund managers now account for roughly 10% of trading volume, down from 80% in the 1990s.

“The trading activity which drives prices is now driven not by active fund management decisions but by the momentum feedback loop of funds moving from active to passive and reweighting within passive funds,” he said.

Against this backdrop, Smith said the first two parts of Fundsmith's investment mantra, buying good companies and not overpaying, remain unchanged. The third element – ‘do nothing’ – is the one under revision.

Fundsmith Equity's turnover reached 51.8% in the period, although Smith said investors should not expect this level to persist. Voluntary dealing, meaning trades not caused by subscriptions or redemptions, cost the fund £11,404,962 during the half year, equivalent to 0.084% of assets.

Explaining the shift, Smith wrote: "In a market in which share price moves of 33% per day for even large stocks are not uncommon a buy and hold strategy can only work if you are not subject to flows, and we are.

“Sticking to our current approach may well fall foul of the adage that the market can remain illogical longer than we can remain in business. You should therefore expect that we will be more active in future. I still expect our turnover and its cost to be significantly below that of most active funds, but it may well be higher than our historic average.”

Performance of Fundsmith Equity vs sector and index in H1 2026

Source: FE Analytics. Total return in sterling between 1 Jan and 30 Jun 2026

The manager said the fund will take more account of momentum — both fundamental and share price — when making investment decisions. Smith will also place less weight on a technique he has used before: buying shares in quality companies after they suffer a setback. He compared this to catching "the proverbial falling knife" in the current market.

He added: "All we are getting is cut fingers as their downward share price spiral is exacerbated by the index momentum enhancement effect."

Smith was clear that the fund's changes do not amount to tracking the market. "We have no desire to hug the index," he wrote. "You can buy index funds that are much cheaper than us or any other active manager, so what would be the point?"

Fundsmith Equity opened new positions across six sectors during the period. In industrials, it initiated stakes in GE Vernova, Legrand, Nextpower and Uber.

GE Vernova builds and services gas turbines and grid equipment. Smith highlighted an order backlog of $163bn, equivalent to four times 2025 revenues, and noted the company's small modular nuclear reactor project under construction in Canada, due for completion by 2030.

Legrand, a French manufacturer of electrical and digital building infrastructure, holds close to 20% global market share in wiring devices. Smith said growth would come from rising demand for energy-efficient buildings and power systems for data centres.

Nextpower makes systems that let solar panels track the sun, which Smith said increases energy yield by 20% to 30% compared with fixed installations. The company acquired battery maker Prevalon Energy for $365m in May 2026 to expand into data centre applications.

Uber was added on the view that network effects between drivers and riders have strengthened as rival ride-hailing platforms have exited the market. The company's operating cashflow rose from a loss of $4.3bn in 2019 to more than $10bn in 2025.

In financials, Fundsmith Equity bought Mastercard, which it now holds alongside Visa. Smith said the two companies are "equally good businesses" and that owning both gives the fund over 6% exposure to payments without excessive stock-specific risk.

The fund's healthcare purchase was Veeva Systems, whose cloud software manages clinical trials and manufacturing compliance for drugmakers. Smith said the company holds roughly 80% market share in pharmaceutical customer relationship software, supported by high switching costs.

In information technology, the fund bought AppLovin, Sage and TSMC. AppLovin's platform serves more than 1bn daily active users and, Smith said, generates more advertising revenue than Snap, Pinterest, Reddit and X combined, driven by its AXON ad-matching engine.

Sage replaced Intuit in the portfolio. Smith said the accounting software company carries less reliance on share-based compensation and lacks Intuit's record of "injurious acquisitions".

TSMC, the world's largest contract chipmaker, manufactures roughly 90% of the world's most advanced semiconductors, a position Smith said is protected by the estimated $20bn cost of building a single advanced factory.

In consumer discretionary, the fund bought The TJX Companies, parent of TK Maxx and Marshalls, citing its network of more than 1,400 buyers sourcing from 21,000 vendors.

It also bought Yum! Brands, owner of KFC and Taco Bell, noting the pending sale of Pizza Hut, which Smith described as "a significant drag on overall results".

The sole communication services purchase was Netflix. It now accounts for nearly 8% of all television screen time in the United States, pointing to growth in its advertising tier and a crackdown on password sharing that added 41m subscribers after being introduced in 2024.

On the sell side, Unilever prompted the longest explanation in the letter. Smith said Fundsmith had supported former chief executive Hein Schumacher's stated plan to avoid acquisitions or divestments until existing businesses were performing to standard, a commitment abandoned after Schumacher's departure.

Following the ice cream business's separation as Magnum Ice Cream Company, Unilever announced plans to transfer its food business to McCormick, a move Smith linked to activist investor Nelson Peltz.

Smith explained: "We are not fans of the idea that corporate activity solves fundamental problems. Nor are we fans of boards who listen to activists who are not long-term investors."

He also noted that "the structure of the deal means we don't get to vote on it".

Novo Nordisk was sold after the company, according to Smith, "parlayed a market-leading position in the biggest drug discovery in decades into an investment disaster".

Nike was sold on the view that a turnaround under new chief executive Elliott Hill would take longer than expected, given ongoing problems in China and at Converse. Zoetis was sold over what Smith described as management's inability to respond to new generic competition or communicate clearly.

Other disposals, including Atlas Copco, Coloplast, EssilorLuxottica, Intuit, LVMH, Magnum Ice Cream Co., Mettler-Toledo, Otis and Wolters Kluwer, were driven by a range of company-specific factors: slowing growth, valuations Smith judged too high, acquisition missteps and, in Magnum's case, a position too small and illiquid for the fund to build meaningfully.

The resulting portfolio carries a return on capital employed of 31%, a gross margin of 62% and a free cashflow yield of 4.3%, against an estimated free cashflow yield below 2% for the S&P 500. Smith expects these companies to grow cashflow by about 14% a year over the next three to five years, adding that they would either become more lowly valued or see share prices rise to reflect that growth.

Smith gave no timeline for when current market conditions might change, saying: “I profess no insight into how or when this passive-led momentum market will end, other than to say badly.”

“More likely it is something which we cannot foresee. After all a crisis would not be a crisis if we could foresee it. But we do know that trees do not grow to the sky,” he added.