European mid-caps have been the strongest part of the region’s equity market over the past decade, recent Trustnet research found, and market experts believe the segment is well-placed to continue outperforming.

As such, Trustnet asked fund selectors to identify funds and investment trusts they believe offer meaningful exposure to Europe’s blossoming mid-sized businesses.

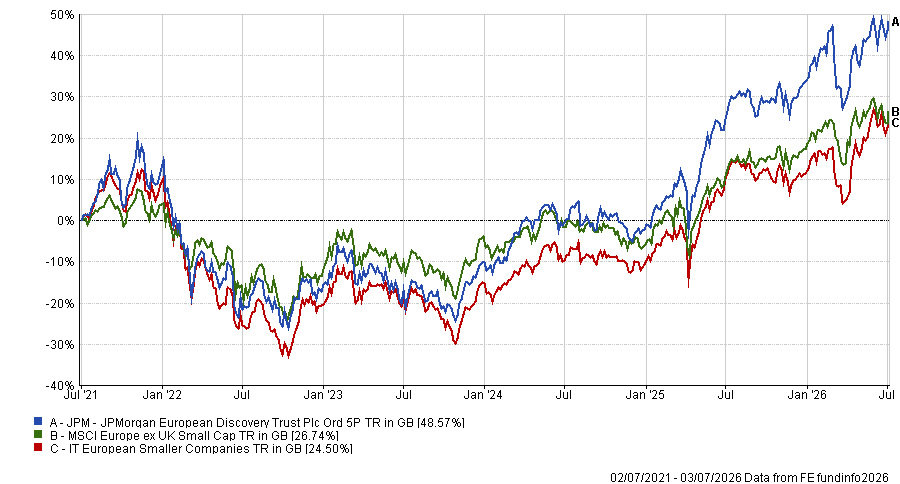

First up, Billy Ewins, fund research analyst at Quilter Cheviot, suggested the £585m JPMorgan European Discovery Trust, noting that it provides differentiated access to Europe’s small- and mid-cap universe through a disciplined and high-conviction investment process.

As of 31 May 2026, over 80% of JPMorgan European Discovery Trust was invested in European mid-caps, with 13.3% in small-caps and just 3.6% in large-caps.

“The trust stands out for the experience of its team, long-term performance track record and its proven ability to identify underappreciated businesses with strong fundamentals,” Ewins said.

The managers – Jack Featherby, Jonathan Ingram and Jules Bloch – are bottom-up stock pickers, combining quantitative screening with fundamental research to identify companies with attractive valuations, improving business quality and positive earnings momentum.

The trust has posted a first-quartile one, three and five-year return against the IT European Smaller ex UK sector, gaining 16.6%, 75.3% and 46.9% respectively.

Rob Morgan, chief analyst at Charles Stanley, also picked JPMorgan European Discovery Trust, noting that its structure and ability to gear should offer an advantage over open-ended competition.

“It is an interesting higher risk proposition for investors seeking capital growth from an often-overlooked asset class – [although] given the risk profile of both the asset class and the greater volatility involved in a trust that can employ some gearing, this is best held in a smaller portfolio position size, perhaps complementing a more mainstream European equities fund devoted to larger stocks,” Morgan said.

The trust is currently trading at a 6.5% discount to net asset value (NAV).

Performance of the trust vs sector and benchmark over 5yrs

Source: FE Analytics

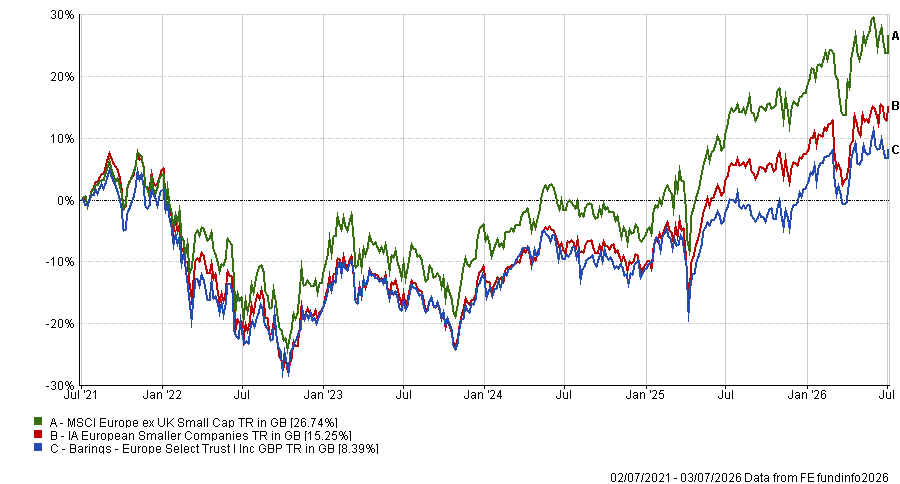

Meanwhile, Kate Marshall, head of fund research at Hargreaves Lansdown, pointed to Barings Europe Select, which is on the investment platform’s Wealth Shortlist.

While the fund predominantly invests in smaller businesses, it invests in companies with a market capitalisation ranging from $456m up to $19.4bn in size, with a meaningful weighting to mid-sized businesses.

Marshall highlighted the experience and longevity of the fund’s lead manager, Nick Williams, who took over the fund in 2005 and has amassed over three decades of experience investing in Europe.

Under Williams’ management, the fund has gained 772.8% to the end of May 2026, according to Marshall.

Williams utilises the growth at a reasonable price (GARP) philosophy, identifying companies in good financial shape, with low levels of debt and a quality management team, only investing in stocks he believes can increase the existing stock price by 40%.

If the share price of a portfolio holding instead falls by 20%, the stock is sold.

“There aren’t many fund managers with such a long and successful track record of investing in this area,” she said.

The fund has nonetheless underperformed the MSCI Europe ex UK Mid Cap index over the past decade, as its focus on quality has been a headwind.

Indeed, looking at discrete annual returns, the fund has lagged in the third quartile in 2023, 2024 and 2025. Although in the second quartile for returns in the sector in 2022, it made a loss of 18.6%.

Despite the near-term performance challenges, Morgan also highlighted the fund, noting that “the experience of the team and consistent application of a repeatable investment process makes it a worthy consideration in the European small- and mid-cap space”.

Both Morgan and Marshall said the fund is likely to take more of a satellite position in an investor’s portfolio, due to the increased level of risk attached to investing in smaller companies.

Performance of the trust vs sector and benchmark over 5yrs

Source: FE Analytics

Darius McDermott, managing director at FundCalibre, highlighted both IFSL Marlborough European Special Situations and Montanaro European Income.

The former is a £167m strategy managed by FE fundinfo Alpha Manager David Walton – supported by Tom Livesey and Steve Robertson – that targets outperformance of the benchmark over a minimum of five years.

McDermott said: “It is a true stock picker’s fund focused on under-the-radar European businesses that larger peers tend to overlook, with a bias towards small- and mid-cap stocks.”

However, unlike the earlier funds, it has a much higher weighting to small- and micro-caps at 37.2% and 26.2% respectively, while 9.8% of the fund is invested in mid-caps.

Although the fund has vacillated between the third and second quartile for returns against its peers over one, three and five years, it has ultimately posted a first-quartile return of 211.7% over the decade.

Then McDermott said that the smaller €77m Montanaro European Income fund “provides a stable and growing income stream with a focus on the continent’s under-researched small- and medium-sized companies”.

The strategy is managed by Alex Magni, supported by George Cooke, and targets capital growth alongside income. It typically holds 50 stocks, with around one-third in mid-caps and two-thirds in small-caps.

As of 29 May 2026, the majority (31%) of the portfolio was invested in companies with a market capitalisation between £1bn to £2.5bn, 17% in companies in the £2.5bn to £5bn range and 16% between £5bn to £10bn.

The Montanaro strategy also has a bias towards quality-growth businesses, a style that has lagged in recent years.

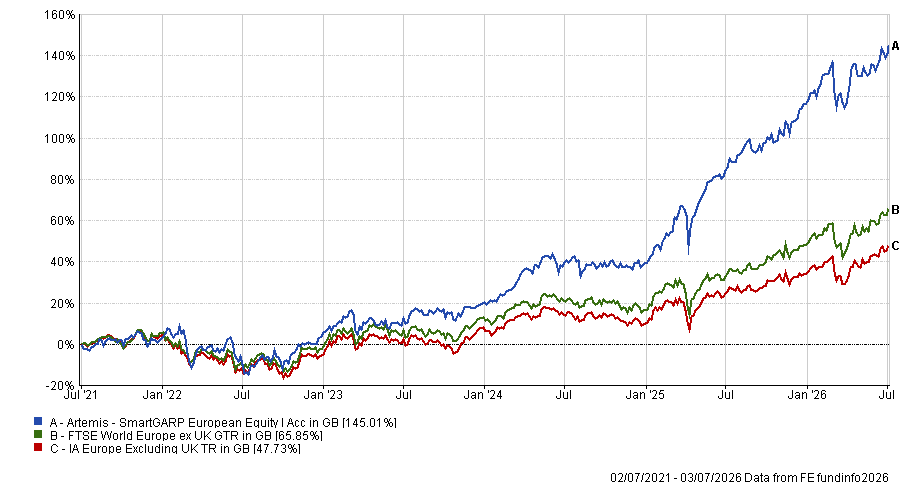

In contrast to the other fund selectors, Dzmitry Lipski, head of funds research at interactive investor, suggested a less obvious fund for European mid-cap exposure: the £2bn Artemis SmartGARP European Equity fund.

“Unlike many European equity funds that are more growth or large-cap oriented, this strategy is different: value-oriented with mid-cap bias,” he said.

As an example, in May Alpha Manager Philip Wolstencroft said he had reduced positions in large-caps such as insurance firm Mapfre and recycled the proceeds into mid-cap stocks such as Nordex, a European company that designs, sells and manufactures wind turbines, citing the need “to ensure the fund owns attractively valued stocks with earnings upgrades”.

This also speaks to Artemis’ proprietary SmartGARP process, designed by Wolstencroft, which is a quantitative analysis tool that screens the financial characteristics of companies, identifying those that are valued materially lower than their growth prospects merit.

“Artemis SmartGARP European Equity is a viable core holding in a global well-diversified portfolio, with a competitive ongoing charge of 0.82%,” Lipski added.

The fund has also consistently outperformed, logging first quartile returns in the IA Europe Excluding UK sector over one, three, five and 10 years – gaining 272.3% over the decade.

Performance of the trust vs sector and benchmark over 5yrs

Source: FE Analytics