For many years Asia has been viewed an attractive region to invest in given its superior rates of economic growth and large and growing populations, including two of the world’s largest countries in India and China.

However, as anyone who has invested in China will tell you, economic growth and large populations don’t always result in superior stock market returns over the long term.

But what regions and markets are investors really getting exposure to within an ‘Asia’ allocation?

Variety of indices

Despite the Investment Association (IA) seeming to neatly split the Asian region into sectors, including and excluding Japan, the underlying indices of funds within the region are broad and varied.

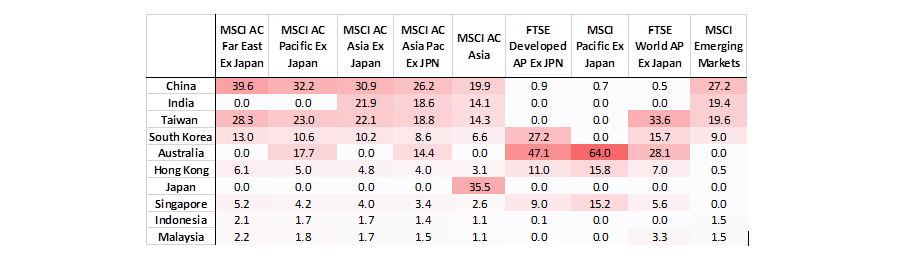

In the table below, we show the country exposures of various Asia benchmarks, and you’ll see that both the number of indices, and the difference in allocations to China, India, Taiwan and Australia, are stark.

Country weighting of Asia benchmarks

Source: AJ Bell

Whilst not as stark, the variance in sector allocations between the indices is also notable, with Asian developed markets typically associated with lower technology and higher financial services and basic materials exposures.

Whilst the composition of a benchmark is most pertinent for passive investing, it is also a telling feature for active funds, as the choice of index typically shows what a manager perceives their most fitting opportunity set to be.

Across such a diverse asset class and with such a variety in indices, peer group analysis becomes more difficult to assess due to the different structural weights that funds have.

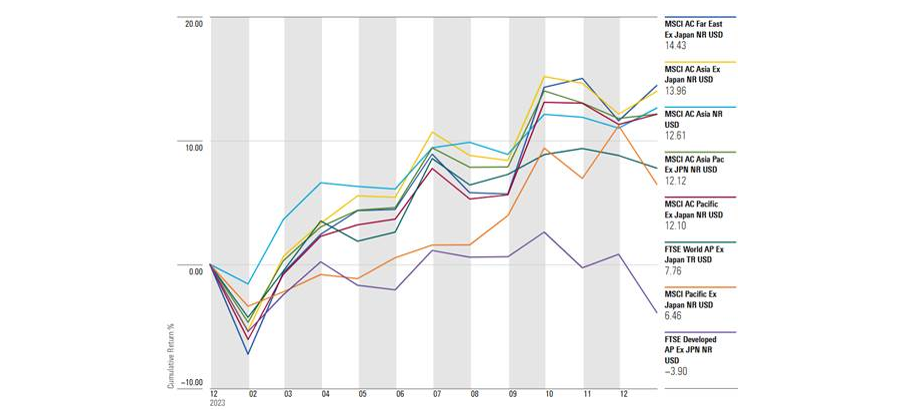

The chart below demonstrates this challenge to sector-relative performance analysis, showing an 18 percentage point spread in total returns between the region’s best and worst performing indices in 2024.

Returns of Asian indices in 2024

Source: AJ Bell

As ever it is therefore important to understand the most appropriate index for any individual fund and consider its relative returns accordingly.

Asia funds investors may consider

At the start of 2025 we shifted our allocation to the Asia region within the AJ Bell portfolios to a mixture of emerging markets excluding China and dedicated China funds, which, whilst broader than a direct Asia fund, include a large weighting towards Asian countries.

We do however use Developed Asia Pacific strategies as these tend to not double up our exposure to emerging market ex China and China holdings. Elsewhere within our business we continue to favour broader Asia Pacific funds.

Jupiter Asian Income

Lead manager Jason Pidcock has been a stalwart of the sector for many years having worked at Newton prior to joining Jupiter in 2015. He invests across Asia, including Australia, however his long-term pessimistic view of China has resulted in a structural underweight to the country, which differentiates the fund from many of its peers.

The manager’s investment approach looks to target companies with strong management teams and a sustainable advantage in their industry, which should allow them to pay out enhanced dividends thanks to the superior cash they generate.

The manager seeks to achieve a total return ahead of the FTSE All World Asia Pacific Ex Japan, a benchmark with characteristics akin to the MSCI AC Asia Pacific index, through both capital growth and an income generation in excess of 120% of the index.

Invesco Asian

The Asian and emerging market franchise at Invesco is underpinned by a clear investment approach honed over many years. Named lead manager, and co-head of the team, William Lam, has more than two decades of investment experience, most of which has been spent focusing on Asian equities.

Central to the team’s philosophy is the belief that markets are too focused on short-term news which leads companies to be mispriced. Ultimately, the fund manager is seeking companies trading at significant discounts to the team’s estimated fair value, targeting a double-digit annualised return from each stock.

The fund is managed with a contrarian mindset, with the team seeking to outperform the MSCI AC Asia Pacific Ex Japan.

Stewart Investors Asia Pacific Leaders

Despite a recent change to the fund’s name, the investment approach, which has been in place for many years, remains unchanged. Fund manager David Gait learnt his trade under the tutelage of well-respected veteran fund manager, Angus Tulloch, and has nearly three decades of investment experience.

The team look to identify high quality companies and hold them for the long term. Sustainability is an important component of their quality criteria, with the managers believing companies with higher sustainable credentials will be those that offer better durability of earnings. The team do not pay careful attention to indices, so performance can be variable versus the market.

Vanguard FTSE Developed Asia Pacific ex Japan UCTIS ETF

For investors who want to passively invest in the developed regions of Asia, they can do so via the Vanguard FTSE Developed Asia Pacific ex Japan ETF. This index captures the large and mid-cap segments of the developed markets in the Asia and the Pacific Region, excluding Japan.

Unlike MSCI, FTSE class South Korea as a developed market, meaning investors holding this fund alongside a position in emerging markets need to be mindful of the index on their emerging markets position to avoid an excessive holding in South Korea.

The fund is a physically replicating fund, carries a competitive OCF of 0.15% and has tracked its benchmark well over a long time horizon.

Paul Angell is head of investment research at AJ Bell. The views expressed above should not be taken as investment advice.