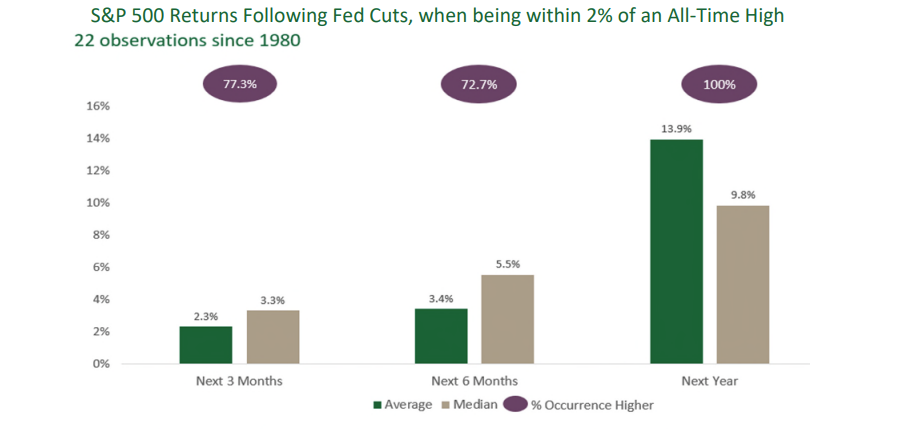

Every time the Federal Reserve has cut interest rates with markets nearing an all-time high, the S&P 500 produced a positive return over the next year.

In over 40 years of market research, that has been true in 100% of cases, with the return averaging 14%, according to research by Carson Investment Research.

As the US has finally entered a rate-cutting environment, retreating would be the wrong move, according to Gerrit Smit, FE fundinfo Alpha Manager of the Stonehage Fleming Global Best Ideas fund, who said “investors should remain invested”.

Source: Stonehage Fleming. Carson Investment Research.

So far, investors have not been following Smit’s advice. The recent Calastone Fund Flows index found £146m pulled from North American funds in the third quarter of 2025, despite the S&P 500 rallying back to form.

Experts are also worried about heightened valuations and expectations that seem to parallel earlier bubbles, with some arguing that the US equity market could return zero in the next few years.

For Smit, however, current conditions in the US seem broadly constructive, meaning that the S&P 500 could be on course for another positive return.

Growth in the US is stronger than expected, with US GDP figures for the second quarter having recently been revised upwards, he noted. While the US is a very consumption-dependent economy, the consumer is in a “decent” position, which could contribute to further outperformance.

“It’s not that corporations and households in America are stretched. Their balance sheets are in a decent position and they could spend if they wanted to – they are just choosing not to,” the manager explained.

Additionally, significant amounts of capital expenditure are still being poured into the US economy, particularly from the artificial intelligence (AI) hyper-scalers and mega-caps.

“Total capital expenditure is already on a high base and accelerating – that’s more money going into the economy, which is clearly supportive for US equities,” Smit said.

He also argued that many investors and analysts have become “far too conservative, despite broadly supportive fundamentals”. Investors, particularly those with long time horizons, were burned by the global financial crisis, where they were too optimistic, and the market’s “appetite for disappointment” has shrunk alongside it.

However, Smit argued they are underestimating the potential for the strongest stocks in the US market to surprise on the upside and continue to deliver strong returns. He pointed to the second quarter of 2025, where many companies beat already-lofty expectations despite concerns over tariffs.

Companies are just far stronger than they used to be, he noted, with strong balance sheets, positive free cash flow and limited debt that makes comparison to the dot-com bubble not entirely accurate.

“Take a company like Microsoft or Alphabet. Despite all the capex they're putting into AI, they still have positive free cash flow, so they don’t really need to worry about debt. That wasn’t really the case in 2001 and 2002,” the Alpha Manager said.

As a result, he has pushed the North American equity allocation within his portfolio to around 79.4%, a 15% overweight compared to the MSCI ACWI.

However, while remaining broadly constructive on US equities, he warned investors not to put all of their eggs in one basket.

Some companies just do not have the free cash flow and strong fundamentals of companies such as Alphabet, with Smit highlighting some of the cloud services businesses as having to “spend fortunes on Nvidia and Broadcom” chips to compete.

Additionally, with currencies such as the Sterling and Euro all performing well, it would pay for investors to diversify their equity exposure to avoid being trapped in one currency and take advantage of some rallying markets elsewhere, he explained.

“I haven’t got any reservations about US exceptionalism. But what I do think is true is that many investors are overinvested in the US and it may pay to start thinking about diversification,” Smit concluded.