South Korea has emerged as one of investors’ favourite regions amid the artificial intelligence (AI) boom but one fund manager cautions that its rapid ascent means the market is now in bubble territory.

Last week, emerging market managers highlighted South Korea as a key market expected to continue driving strong returns in 2026, citing its exposure to the AI value chain and its cheaper valuations relative to developed market peers.

Such conviction has been reinforced by the scale of South Korea’s outperformance in recent years.

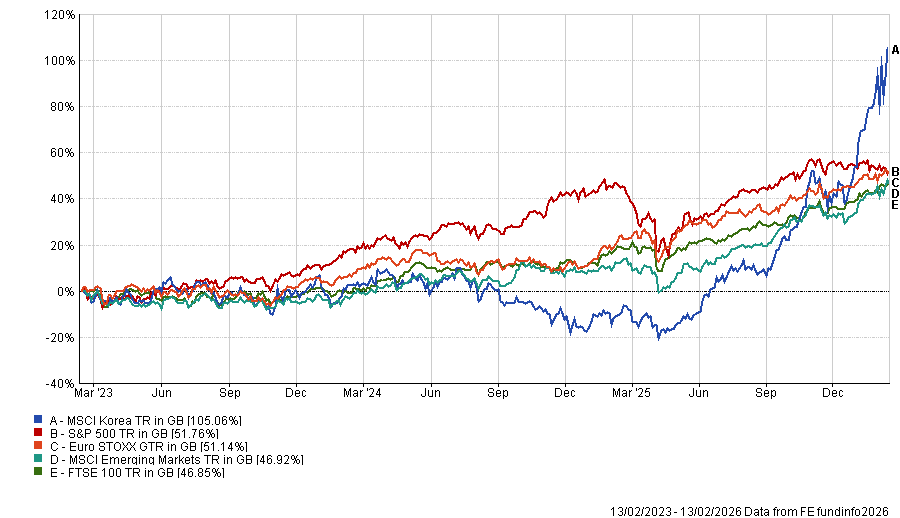

As shown in the graph below, the MSCI Korea index has gained 92.8% over the three years to the end of January, around double the returns made by Euro STOXX, MSCI Emerging Markets, S&P 500 and FTSE 100.

Performance of MSCI Korea vs other major markets over 3yrs

Source: FE Analytics

However, Rob Marshall-Lee, founding partner and chief investment officer at Cusana Capital, countered that South Korea’s rally is built on low-quality businesses and speculative flows, creating a fundamentally unsustainable market.

“South Korea is a massive bubble,” he said. “I wouldn’t necessarily bet against the market on a one-year view, but on a five-year view you will probably lose a lot of money.”

He added that there used to be a value case for South Korea “but there has never been a quality case”.

Marshall-Lee’s underlying concern is that too many Korean stocks have seen a tripling in their share price due to tenuous links to AI and not because of profit growth.

“Most Korean companies generate very low returns on equity, so those businesses are not going to magically transform because of AI – Hyundai is up 60% year-to-date simply because it talks about robotics, for example,” Marshall-Lee said.

“If you are buying companies [in the AI hardware space] like SK Hynix or Samsung after their margins have gone from 15% to 70%, you should still expect those margins to normalise again and be questioning how steep the glide path will be.”

In contrast, a company like TSMC in Taiwan, which has a near-monopoly position in the AI hardware market, is far more resilient should the AI bubble burst, according to Marshall-Lee.

“Hynix and Samsung operate in a much more cyclical industry with very limited competitive advantages,” he said.

“When the cycle turns, their margins can collapse from 70% to potentially negative. TSMC might lose you 20 to 30% but certainly not 80% because the underlying business is so much stronger.”

Despite his concerns, Marshall-Lee acknowledged that the macro picture has been more encouraging following the South Korean government’s positive efforts to reform corporate governance. A landmark reform bill passed last year includes measures to enhance shareholder rights and increase board accountability, such as the adoption of cumulative voting for large listed companies and the separate election of audit committee members.

“When the political narrative shifted after the election last year, retail investors poured money in,” he said. “But it’s now a very frothy market and I remain cautious on South Korea in general.”

The Cusana Capital emerging markets equity strategy has a 3% position in the country, but, when looking for AI-related investment opportunities across emerging markets, Marshall-Lee said he favours China over South Korea.

He pointed to China’s efforts to build its own domestic capability in memory chip production – specifically those used in phones, laptops, data centres and AI hardware.

However, he remains selective. For example, he favours Tencent over Alibaba, noting the former “has a really solid business and is spending on AI – but not too much”.

In contrast, an emerging market which has lost out in the AI boom is India, yet Marshall-Lee is more positive on the region over a five-year time horizon.

“On a 12-month trading view, money has been flowing out of India and into the hot areas for AI – South Korea is the poster child there,” he said.

“But many of the best businesses in emerging markets are based in India, and they are still growing by 15% or 20% per annum. Right now, India is an undervalued market with an undervalued currency and is a source of some of the best opportunities over the next five to 10 years.”

The macro picture is also positive, he said, aside from a few “sticking points” – namely tensions with the US over tariffs.

Marshall-Lee noted that India prime minister Narendra Modi’s leadership has been “excellent”, citing the government’s efforts to drive internal growth, as well as making trade deals with developed markets such as the UK and EU – all of which “puts India in a strong long-term position on the global stage”.