Persistent shipping bottlenecks and reserve rebuilding will push Brent crude to $75-80 a barrel over the next six to 12 months, even though it fell after the ceasefire between the US and Iran, according to J. Safra Sarasin Sustainable Asset Management’s Raphael Olszyna-Marzys.

Analysts at Citi expect Brent to fall to between $60 and $65 a barrel by the end of the year, a forecast built on the assumption that the US-Iran truce holds and traffic through the strait of Hormuz continues to normalise. Morgan Stanley expects Brent crude to end 2026 at $75 a barrel, while UBS' forecast is $80.

Olszyna-Marzys, international economist at J. Safra Sarasin Sustainable Asset Management, does not dispute that some normalisation is underway but sees the mechanics of that recovery pointing toward higher prices rather than lower ones.

"The oil forward curve has slipped into mild contango at the very front end: September futures now trade above the spot price for the first time since the war began, suggesting that the market is, at least marginally, oversupplied, pushing down on prices," he said.

The economist expects near-term prices could dip modestly below today's level near $70 before climbing back into the $75-80 range.

His argument rests partly on how little Hormuz traffic actually needs to recover for exports to normalise. Before the war, around 15 million barrels a day of crude passed through the strait, rising to roughly 20 million barrels a day once refined products are included.

Alternative routes have since reduced that dependency, with Saudi Arabia shipping more via its East-West pipeline and the Red Sea, and the UAE routing crude through Fujairah while building a second pipeline that could eventually carry almost all its output without touching Hormuz.

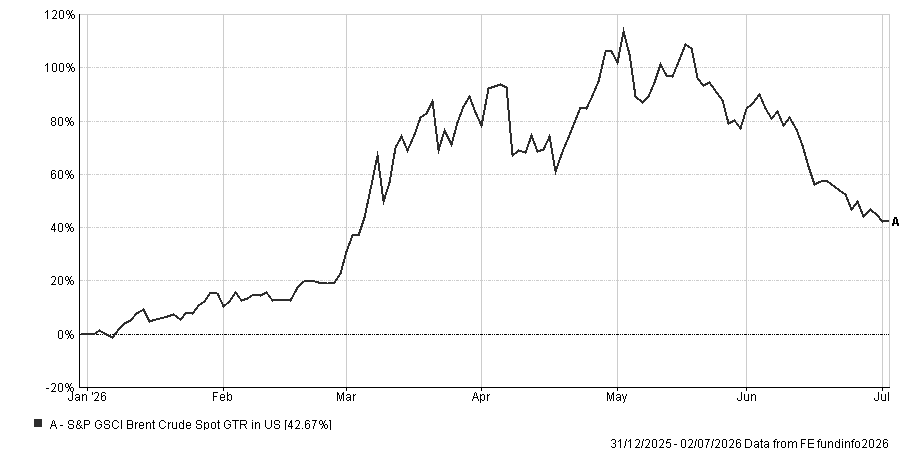

Performance of oil over 2026 in US dollars

Source: FE Analytics

Working through those alternative volumes, Olszyna-Marzys estimates that only around 7.5 million barrels a day of crude would need to transit the strait to restore pre-war export levels from the region. Refined products are harder to reroute: roughly 5 million barrels a day of diesel, petrol and jet fuel still need to leave by sea.

Put together, he judges that flows at 60-65% of former Hormuz levels would be enough to normalise exports, assuming demand holds broadly steady.

But actual traffic remains well short of that mark as total vessel movements through the strait are running at roughly a quarter of pre-war levels and inbound traffic is closer to a fifth.

Olszyna-Marzys puts that gap down to how the recovery has been sequenced so far: "The immediate priority was to allow stranded vessels to leave the Gulf. Empty tankers, many of which have been redeployed elsewhere, will take time to return."

The bigger question is whether traffic can climb back to the 60-65% threshold at all, but he is doubtful it will happen smoothly.

"The situation remains fragile and traffic could struggle to recover to the 60-65% threshold. Ships are avoiding the main shipping lane, parts of which remain mined and instead hugging the Omani coast, where waters are shallower and currents stronger. Tankers continue to rely on protection from the US Navy against intermittent drone attacks."

No full demining operation has yet begun, he added, a process he expects to take months once it starts. "All this suggests that the risk of disruption remains elevated," he said.

Insurance markets appear to agree. Hull war-risk premiums have eased from around 5% of a vessel's value to roughly 2%, but that remains far above the 0.25% level that prevailed before the conflict began.

Demand has its own dynamics feeding into the forecast. China has absorbed much of the shock during the war, drawing down an estimated 400 million barrels from its inventories, comparable to the combined drawdown across all advanced economies.

Olszyna-Marzys expects that pattern to reverse and reinforce prices from here. "Efforts to rebuild, and in some cases expand, strategic reserves are likely to support demand in the coming quarters, placing a floor under oil prices and, if anything, exerting upward pressure on them," he argued.

Even accounting for structural shifts in demand, he sees a persistent gap between supply and pre-war consumption. He estimates that around 1 million barrels a day of demand may have been permanently destroyed through faster adoption of electric vehicles and other efficiency gains, yet considers a full reopening of the strait unlikely.

Using a price elasticity of demand assumption of -0.2, his modelling points to oil needing to settle near $75-80 a barrel later this year to bring the market back into balance.

However, the inflation implications of this, in his view, are manageable rather than alarming: "Compared with pre-war forecasts, higher energy prices are likely to add around one percentage point to inflation.

"Some second-round effects are inevitable, but they should remain limited given the spare capacity that still exists across many European economies. Indeed, inflation in the UK has surprised on the downside in recent months."

Markets initially priced a series of rate increases across Europe in response to the conflict, but those expectations have since been scaled back sharply.

Investors now anticipate only one additional 25-basis-point increase from the European Central Bank, less than one full hike from the Bank of England by year-end and no tightening at all from the Swiss National Bank. Olszyna-Marzys regards this repricing as appropriate.

The picture looks different in the United States, where markets have begun pricing a more hawkish Federal Reserve. He attributes that shift mainly to domestic economic developments rather than to the outlook for oil: "In the US, markets have begun to price a more hawkish Fed. Yet that shift reflects domestic developments far more than the outlook for oil prices."