The AI semiconductor cycle has entered an intermediate expansion phase rather than a bubble or a turnaround, with its future direction resting on whether returns on invested capital by hyperscalers and AI labs keep pace with their spending, Edmond de Rothschild argues.

In a report on the semiconductor and AI investment cycle, the private bank highlighted two trends that are critical to understanding what might happen from here as hyperscalers commit massive sums of money to the ongoing AI build-out.

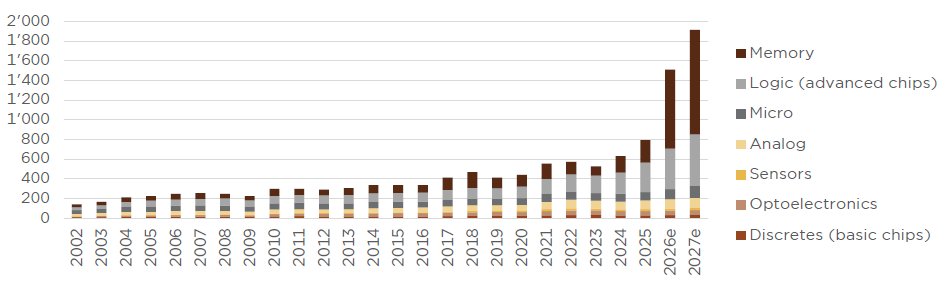

"The first is the unprecedented transfer of value taking place from the balance sheets of hyperscalers to computing hardware manufacturers – and foremost among them, memory manufacturers, whose market is on track to surpass the trillion mark ahead of schedule,” Edmond de Rothschild's strategists said.

"The second is the token economy: as long as tokens remain scarce and their production remains constrained, pressure on critical infrastructure links persists and pricing power remains with those who hold the capacity."

Annual semiconductor sales by underlying market, in billions of dollars since 2002

Source: Edmond de Rothschild, WSTS

Tokens, the basic units an AI large language model reads or generates, behave increasingly like a raw material. Their cost has fallen by roughly 90% since 2023, yet business usage has climbed by around 1,000% over the same period.

Edmond de Rothschild expects token demand to overtake installed processing capacity as early as the second half of 2026, which it treats as a genuine inflection point for the industry's monetisation.

The scale of token usage already looks substantial. Several hundred companies are estimated to consume more than a trillion tokens a year and the bank projects total token consumption could rise by a factor of 20 to 30 between 2026 and 2030 as agent-based applications spread.

Price pressure is now visible downstream too. Apple raised prices across its Mac and iPad ranges in late June, citing a memory shortage tied to AI demand, and Microsoft followed with a price increase on Xbox consoles. Hyperscalers and consumers cannot absorb rising memory costs indefinitely, the report noted, even if a full reversal to pre-AI pricing looks unlikely.

Multi-year supply contracts now cover an estimated 30% to 40% of industry volumes, smoothing the sharp peaks and troughs that have historically made memory unpopular with long-term investors.

"The debate is not 'bubble or no bubble' regarding memory prices, but rather the recognition of a new price regime whose floor is higher than the previous one," Edmond de Rothschild strategists said.

"We view the cycle as being in an intermediate expansion phase, nearing a certain level of maturity, rather than a turnaround,” strategists said. “However, the phase of indiscriminate expansion, during which sector exposure alone was sufficient, appears to us to be behind us."

Edmond de Rothschild has adjusted its exposure across the AI value chain, favouring selective positions in upstream segments such as memory, equipment manufacturers and foundries. It described them as facing bottlenecks and holding "defensible pricing power" but added a note of caution on valuations, saying some subsectors already reflect "highly optimistic expectations".

The bank also has selective exposure to hyperscalers, choosing those it judges best positioned on AI technology and infrastructure deployment, and whose end markets support direct AI deployment at scale.

It has turned more cautious on GPU and ASIC designers over the same horizon. Nvidia, Broadcom, AMD and Marvell are increasingly viewed as pass-throughs for memory costs rather than independent sources of margin, which the bank expects to pressure their pricing power.

Software companies remain an area of scepticism, particularly the segments most exposed to disruption from agentic AI.

Adoption of AI, however, still trails previous technology cycles by conventional measures. The private bank noted that AI investment as a share of US GDP remains below the levels reached during the rollout of railroads, electrification and 1990s telecoms infrastructure, and that more than 80% of the AI-related investment expected by 2028 has yet to occur.

Supply-side bottlenecks are expected to ease only gradually. Equipment delivery times, a persistent constraint on capacity expansion, are projected to normalise by mid-2027, while the tight cycle in DRAM memory is expected to run until the second quarter of 2028 and NAND until the end of 2027.

"The key signal to watch will emerge at the intersection of several indicators: the supply-demand balance for token capacity and the underlying electrical power, the sustainability of the absolute level of memory demand as supply increases, the normalisation of equipment lead times expected by mid-2027, the actual monetisation trajectory of hyperscalers, their ability to finance the cycle without damaging their credit profiles, and the dynamics of earnings revisions relative to the multiples paid," Edmond de Rothschild strategists said.

"It is the combination of these signals – rather than any one of them taken in isolation – that we believe will indicate whether the cycle is entering a phase of sustainable consolidation or approaching a turning point. Based on our current analysis, we remain positive on the duration of the investment cycle, while keeping in mind that its direction in the stock market will ultimately depend on the actual returns from these investments."

Beyond the current spending wave, the report points to six factors it expects to extend the cycle further: the continued rise of agent-based AI; energy and data-centre constraints; expansion into physical infrastructure such as cooling and construction; evolving financing structures; sovereignty and defence-related demand; and the fact that broader business adoption remains at an early stage.

Edmond de Rothschild also laid out three scenarios for how this could unfold. In the base case, chip demand holds steady and returns on investment gradually justify the spending, even as capital expenditure runs higher than currently expected.

In an optimistic case, demand proves broader than assumed, extending well beyond hyperscalers into enterprise, edge and sovereign computing, with the massive spending validated by monetisation. But in the pessimistic case, AI revenue growth fails to keep pace with capital spending, memory prices prove unsustainable for downstream buyers and new capacity due after 2028 tips the market into oversupply.