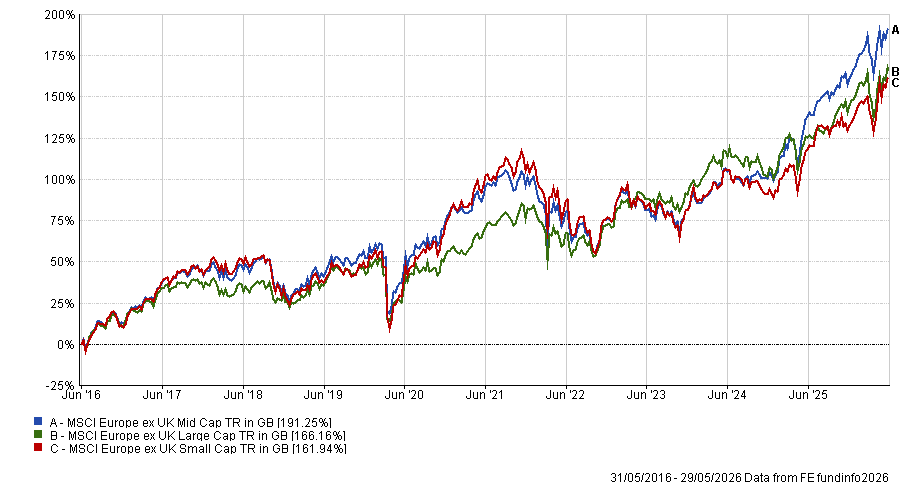

European mid-caps have bucked the trend of the past 10 years, outperforming both small- and large-caps in the region, according to Trustnet research.

The research found that large-caps dominated over the assessed period in all regions bar Europe, where MSCI Europe ex UK Mid Cap gained 191.3%.

Performance of European small-, mid- and large-caps over 10yrs ending 31 May 2026

Source: FE Analytics

The overarching reason for mid-cap outperformance boiled down to what the European market lacks: a concentrated stock-pool of mega-cap tech stocks. This means European large-caps have missed out.

Darius McDermott, managing director at FundCalibre, said: “In the US, Japan and Asia, technology – and more specifically AI – has been the defining trade with as much as 40% of the S&P 500 now reliant on the AI theme.”

In comparison, Europe’s large-caps are dominated by consumer staples, healthcare and luxury goods – sectors that have had a mixed decade.

“Even Novo Nordisk, once a crown jewel of European equity markets, has fallen from nearly €1,000 to around €300 a share, yet it remains the second-largest stock in Europe,” he noted.

“That lack of renewal at the top demonstrates why the dynamism in European markets currently sits further down the cap scale.”

In contrast, McDermott expects the trend of AI large-cap dominance to “only rise when Anthropic and OpenAI eventually join the market”.

While Europe’s large-caps have been weighed down by companies that have struggled to compete with the AI-driven rally, its mid-caps have benefited from a broader and more dynamic mix of industries that has proven resilient in comparison.

Mike Clements, manager of VT Tyndall European Unconstrained, said: “Europe is a good picks and shovels way to play many themes related to AI and data centres, and these have often been found in small- and mid-caps.”

He highlighted Soitec as an example – a France-based manufacturer of substrates used in the manufacturing or semiconductors.

The stock has a market capitalisation of around €4.1bn and its stock price has increased by more than 350% year-to-date.

Stock price performance YTD

Source: Google Finance

More broadly, the region is heavily weighted towards financials, industrials and healthcare, industries that have performed more strongly in the face of ongoing volatility and uncertainty driven by issues such as US tariffs.

Barry Glavin, head of the equity investment platform at Amundi, also pointed to new fiscal initiatives in Europe on defence, infrastructure and energy independence, which has most benefited domestically oriented companies.

“In general, the mid-cap universe is more domestic and therefore tilted to benefit from this,” he said.

Lisa Wang, head of EMEA investment strategy at Franklin Templeton Investment Solutions, also pointed to business structure.

“Some large European industrials remain diversified, multi-division groups that investors may value below the sum of their parts because of complexity, trapped capital or perceived capital allocation inefficiency,” she said.

“More focused mid-cap businesses with clear exposure to long-term themes can be easier for investors to identify and value their growth potential.”

In addition, European mid-caps sit in an attractive stage of the corporate lifecycle, in that they are large enough to benefit from established customer relationships, global reach and proven profitability, while still small enough to deliver above-average growth, she added.

Breaking down the decade

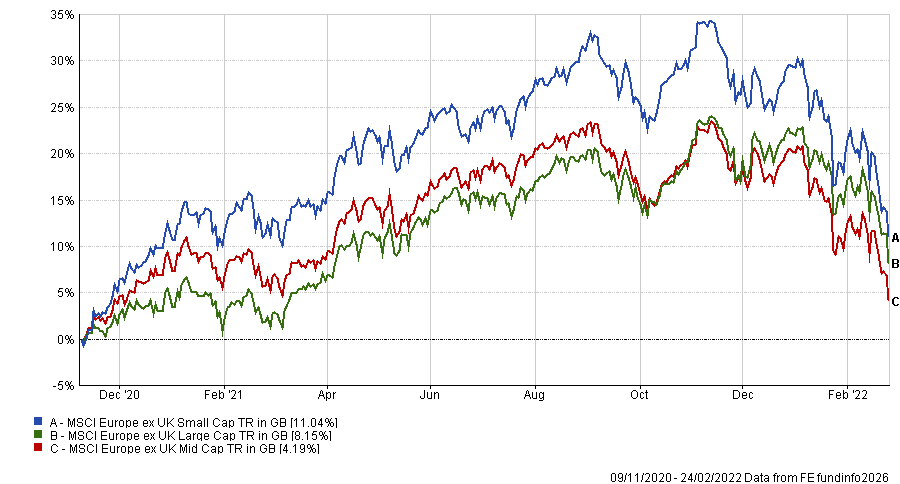

However, mid-caps were not the strongest section of the market throughout the 10-year period. As pointed out by Clements, in the period from the end of the first and most prominent wave of Covid to the start of the conflict between Russia and Ukraine, European small-caps outperformed while mid- and large-caps struggled.

“This was when global supply chains were still a mess, causing the larger, more global companies a logistical headache, while small-caps with their more domestic focus were benefiting from a surge in spending whilst sidestepping some of the logistics issues,” Clements said.

Performance of European small-, mid- and large-caps between Covid and Ukraine war

Source: FE Analytics

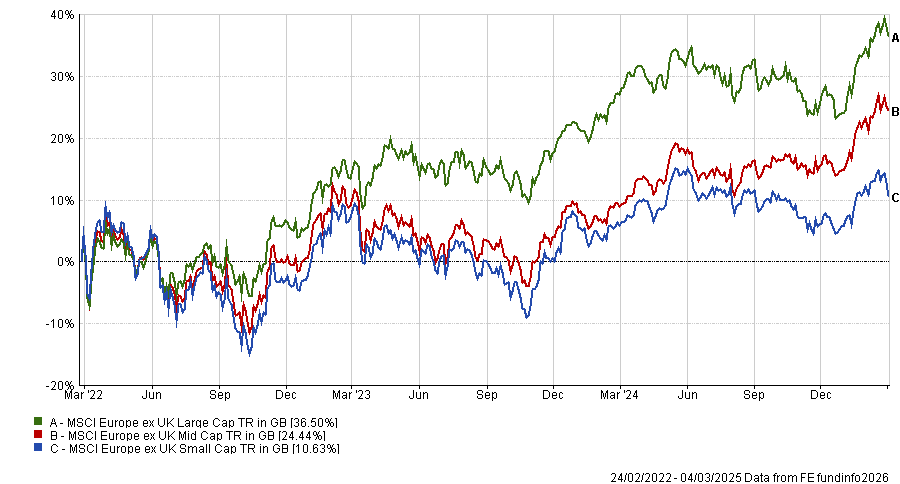

In contrast, in the following three-year period, up to the election of Friedrich Merz as chancellor of Germany on 6 May 2025, renewed uncertainty around European geopolitics and surging energy costs prompted investors to prioritise the global nature and natural liquidity in European large-caps.

Performance of European small-, mid- and large-caps from war in Ukraine to the election of Friedrich Merz

Source: FE Analytics

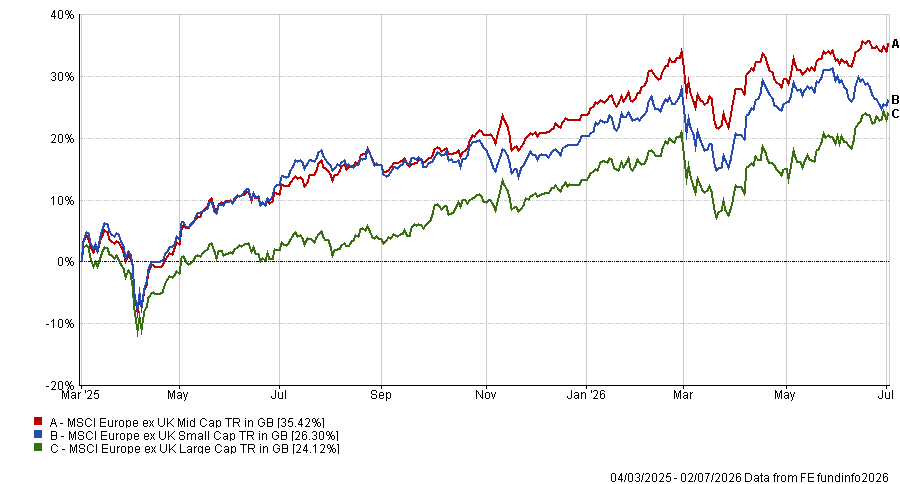

There was then a shift in market sentiment around the time of Merz’s election, when the new chancellor announced plans for the €500bn infrastructure and defence fund which was funded by relaxing Germany’s long-standing fiscal debt brake.

“Ever since this moment, we have seen European small- and mid-cap stocks stage a strong recovery as they are likely to be the main beneficiaries of this surge in spending across the continent,” Clements said.

Performance of European small-, mid- and large-caps since the election of Friedrich Merz

Source: FE Analytics

Will this trend continue?

Managers said European large-caps are unlikely to overtake small- and mid-cap performance in the medium-term, as the shift towards European sovereignty, reshoring of supply chains and the surge in investment into defence and infrastructure favours mid-sized businesses.

“Many of the companies providing specialist components, equipment, software and engineering services sit in the mid-cap segment and could benefit from a broader capital expenditure cycle,” said Wang.

“AI could also create value through its adoption across industrial, healthcare and service businesses as mid-caps with proprietary expertise could be well-placed to benefit.”

However, competition from China in higher-value manufacturing remains a significant challenge, Wang warned, while energy costs and the broader economic backdrop will also determine longer-term success.

In addition, there is simply more headroom, as small- and mid-caps continue to trade at a discount to large-caps on price-to-earnings (P/E), whereas they have historically traded at a premium.

“Earnings growth tends to be higher and balance sheets have improved significantly over the last decade,” Glavin said. “So, we see a strong case for European small- and mid-caps to continue to perform well.”